1 PowerPointPresentation by PowerPoint Presentation by Gail B. Wright Professor Emeritus of Accounting Bryant University © Copyright 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star Logo, and South-Western are trademarks used herein under license. MANAGEMENT ACCOUNTING 8 th EDITION BY HANSEN & MOWEN 4 ACTIVITY-BASED PRODUCT COSTING

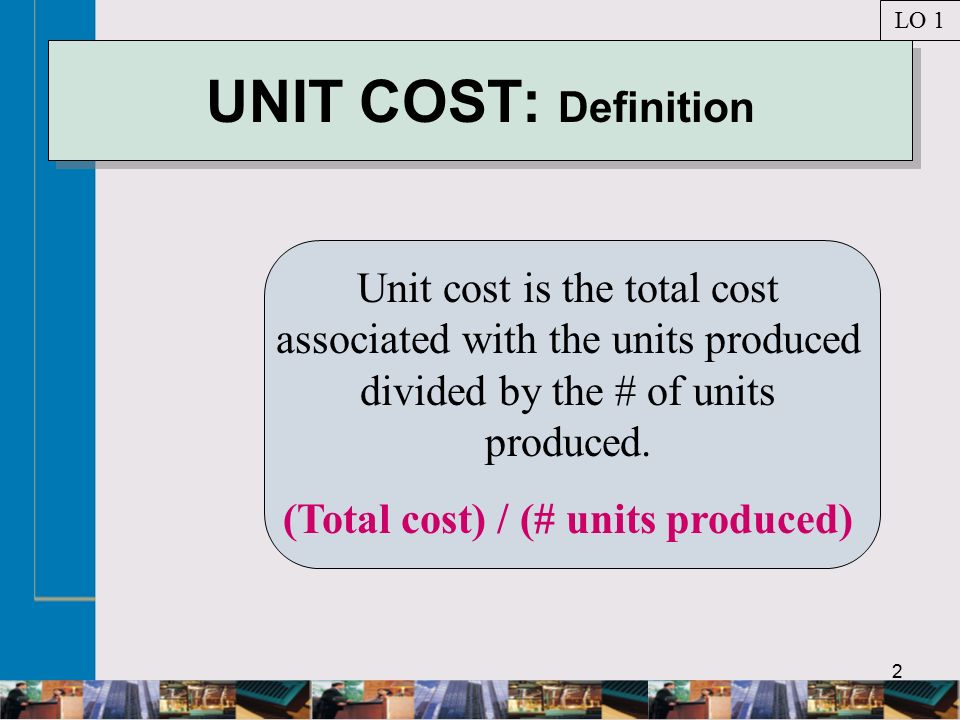

2 UNIT COST: Definition Unit cost is the total cost associated with the units produced divided by the # of units produced. (Total cost) / (# units produced) LO 1

3 What is meant by “total cost”? Total cost refers to production costs: direct materials, direct labor, manufacturing overhead. LO 1

4 How do we measure the costs to be assigned? Production costs we assign may be actual or estimated costs. LO 1

5 How do we assign costs to a product? Production costs are assigned by 1 of 2 methods: functional- based or activity-based costing. LO 1

6 UNIT COSTS Pengaruh Menyerahkan penawaran yang berarti tanpa mengetahui biaya per unit tidak mungkin Mangembangkan dan Memperkenalkan produk baru Keputusan terhadap Membuat atau membeli suatu produk atau jasa Menerima atau menolak pesanan khusus Mempertahankan atau menghentikan suatu produk LO 1

7 UNIT COST INFORMATION Kemungkinan dihitung dengan Actual costing : bahan baku langsung, TK langsung dan Overhead Normal costing Membebankan biaya aktual DM dan DL tetapi OH dibebankan pada produk dengan menggunakan tarif perkiraaan LO 1 Predetermined rate (Tarif Perkiraan OH) = Budgeted cost / Estimated activity usage

8 How are functional-based costs assigned? Direct materials & labor are assigned by direct tracing. Overhead is assigned by driver tracing & allocation. LO 2

9 UNIT-LEVEL DRIVERS Digunakan untuk membebankan OH Unit yang diproduksi Jam tenaga kerja langsung Biaya tenaga kerja langsung Jam mesin Biaya bahan baku langsung LO 2

10 CAPACITY LEVELS: Definition Expected activity capacity is output for coming year Normal activity capacity is average activity experienced over long term Theoretical activity capacity is absolute maximum that can be achieved in perfect world Practical activity capacity is maximum that can be achieved under efficient operation LO 2

11 What does the relationship of capacity levels look like? LO 2 EXHIBIT 4-1

12 PLANTWIDE RATE: An Example Budgeted overhead$360,000 Expected activity (in DLH)100,000 Actual activity (in DLH)100,000 Actual overhead$380,000 Predetermined rate = Budgeted cost / Estimated activity usage = $360,000 / 100,000 = $3.60 per DLH Applied overhead = Overhead rate x Actual activity = $3.60 x 100,000 = $360,000 LO 2

13 What if applied overhead ($360,000) differs from actual overhead ($380,000)? Underapplied (overapplied) overhead is a variance that is added to (subtracted from) cost of goods sold. LO 2

14 PLANTWIDE RATE: 2 Products EXHIBIT 4-3 Similar products use different amounts of labor, so that $360,000 overhead is allocated differently. LO 2

15 DEPARTMENTAL RATE MODEL EXHIBIT 4-4 LO 2 Products produced in different departments use different drivers to assign overhead costs.

16 DEPARTMENTAL RATE: 2 Products EXHIBIT 4.5 Pembuatan banyak menggunakan mesin (bandingkan jam mesin yang diharapkan), sedangkan perakitan cenderung menggunakan banyak tenaga kerja langsung LO 2

17

18

19 How does a company know if its functional-based costing is producing distorted costs? There are many symptoms of distorted costs, such as profit margins that are difficult to explain. LO 3

20 CREATING DISTORTIONS When a unit-level approach is used to assign non-unit-level costs (overhead), cost information can be distorted. LO 3

21 NON-UNIT-LEVEL ACTIVITY DRIVER: Definition Factors that measure consumption of non-unit-level activities by product & can distort product costs. LO 3

22 PRODUCT DIVERSITY: Definition Products consume overhead activities in systematically different proportions. LO 3

23 COST DISTORTIONS: Plantwide Cost Assignment EXHIBIT 4-8 Proportional application assigns 9 times as much overhead to Regular phones. LO 3 } Should we assume that regular phones will use 9 times more overhead costs than cordless phones?

24

25

26 COMPARING UNIT COSTS EXHIBIT 4-11 Activity-based costing is more realistic than functional-based costing. LO 3

27 4 Explain how an activity- based costing system works for product costing. LEARNING OBJECTIVE

28 How do you identify activities & their attributes? Use a key set of interview questions and record the answers. LO 4

29 RESOURCE DRIVER: Definition Factors that measure the consumption of resources by activities. LO 4

30

31 ASSIGNING COSTS TO ACTIVITIES: Step 1 ActivitySupervisorClerks Supervising employees100%0% Processing transactions040 Preparing statements030 Answering questions030% of Time on Each Activity LO 4

32 ASSIGNING COSTS TO ACTIVITIES: Step 2 ActivitySupervisorClerks Supervising employees$50, Processing transactions---$60,000 Preparing statements---$45,000 Answering questions---$45,000 If the supervisor’s salary is $50,000 and each of 5 clerks earn $30,000, costs would be: LO 4

33 How do you assign activity costs? Activity costs are assigned to products on the basis of usage. LO 4

34 ASSIGNING COSTS TO PRODUCTS: Identify Costs ActivityCredit Card Supervising employees$ 75,000 Processing transactions100,000 Preparing statements79,500 Answering questions69,900 Providing automatic tellers250,000 Activity Costs LO 4 EXHIBIT 4-14

35 ASSIGNING COSTS TO PRODUCTS: Assign Costs Activity Classic Gold GoldPlatinumTotal # Cards5,0003,0002,00010,000 Transactions processed 600,000300,000100,0001,000,000 # Statements60,00036,00024,000120,000 # Calls10,00012,0008,00030,000 # Teller transactions15,0003,0002,00020,000 LO 4

36

37