Upload presentasi

Presentasi sedang didownload. Silahkan tunggu

1

Presented by: Dewi Kartika Sari, Dri Asmawanti, Malahayati Sari

2

Introduction Lobbying on FAS 94 Wealth Effects of FAS 94 Adjustments to FAS 94 Consolidation in Canada Conclusions

4

Given no externalities, firms have private incentives to establish accounting policies that maximize both firm value and social welfare. Watts and Zimmerman (1986) recognize, feasible accounting practices are determined not just by private market forces; they are determined through a quasi- political process. This paper seeks further understanding of quasi-political process by focusing on changes in accounting standards governing consolidated reporting.

recognize, feasible accounting practices are determined not just by private market forces; they are determined through a quasi- political process. This paper seeks further understanding of quasi-political process by focusing on changes in accounting standards governing consolidated reporting..")

5

Two general categories of incentives that can be examined regarding consolidation policy: 1. Incentives for choosing whether to report a subsidiary’s performance on a consolidated or an unconsolidated basis given that both are feasible Already address in Mian and Smith (1990a) 2. Incentives associated with changing from one basis to another given a mandated change in the set of feasible accounting provisions.

2. Incentives associated with changing from one basis to another given a mandated change in the set of feasible accounting provisions..")

6

Financial Accounting Standard (FAS) 94. Adopted on 30 October 1987, FAS 94 requires that a firm’s majority-owned subsidiaries be included on a consolidated basis for accounting periods ending after 15 December 1988.

7

Examine whether firms with unconsolidated financial subsidiaries: 1. Are more likely to lobby against the exposure draft for the proposed accounting change, 2. Are more likely to observe a negative abnormal return associated with the announcement of the adoption of FAS 94, 3. Are more likely to engage in transactions that would reduce the cost of FAS 94 compliance.

9

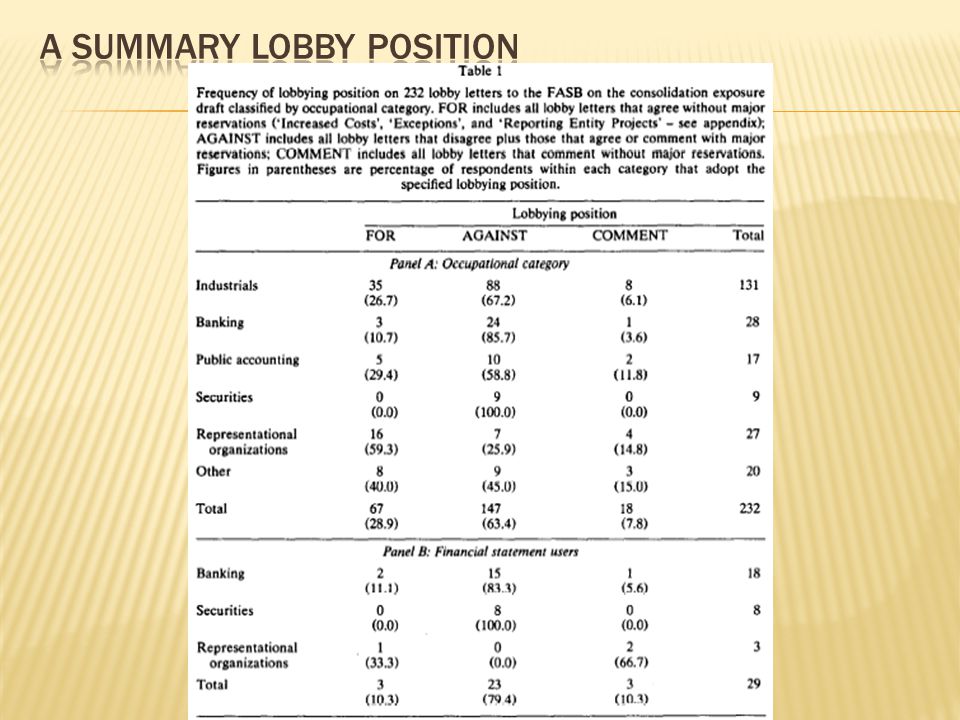

Language in Accounting Research Bulletin 51 allowed managers to report the performance of financial subsidiaries on unconsolidated basis Separate statement or combined statements would be preferable for a subsidiary or group of subsidiaries if the presentation of financial information concerning the particular activities of such subsidiaries would be more informative to shareholders and creditors of the parent company than would the inclusion of such subsidiaries in the consolidation. For example, separate statements may be required for a subsidiary which is a bank or an insurance company and may be preferable for a finance company where the parent and other subsidiaries are engaged in manufacturing operations. In December 1986, the FASB issued an exposure draft of their proposal to eliminate the option to exclude subsidiaries from consolidation on the grounds that their operations are non-homogeneous.

10

Agree without reservation 3M: “We support the issuance of the ED as a final standard. Non-homogeneity should not preclude consolidation of majority owned entities” Agree with reservation Exxon: “However, even though we agree with the board’s basic conclusion in the ED, we take exceptions to certain provisions” disagree General Mills: “We disagree with the proposed statement’s concept of consolidating financial service entities with non-financial parent companies” Comment DuPont: “We express no view with respect to the basic thrust of the ED that all majority- owned subsidiaries should be consolidated unless control is temporary or does not rest with the majority owner, but we offer the following comments on other provisions of the ED for your consideration”

11

1. Time extension Navistar 2. Use of cost method IBM 3. Continued Unconsolidated Disclosures Exxon 4. Increased Costs Marined Midland Bank 5. Exceptions Gulf States Utilities 6. Reporting Entity Project Hewlett Packard

13

The FASB argues that firms’ financial subsidiaries are typically more highly levered than those engaged in manufacturing. By not consolidating, firms show lower leverage than they would if the subsidiaries were consolidated. They argue that this off-balance-sheet financing is potentially misleading to users. This implies that potential users (e.g., the banking and securities industries and risk-rating firms) should be more likely to lobby for FAS 94. Mian & Smith (1990a) suggest an alternate hypothesis: that potential users of accounting statements prefer to have more disaggregated information. This hypothesis implies potential users would lobby against FAS 94. Based on Table (1): 3 lobby FOR 23 lobby AGAINST 3 COMMENT There appears to be little support for the hypothesis that the use of unconsolidated reporting is misleading or confusing.

should be more likely to lobby for FAS 94. Mian & Smith (1990a) suggest an alternate hypothesis: that potential users of accounting statements prefer to have more disaggregated information. This hypothesis implies potential users would lobby against FAS 94. Based on Table (1): 3 lobby FOR 23 lobby AGAINST 3 COMMENT There appears to be little support for the hypothesis that the use of unconsolidated reporting is misleading or confusing..")

14

Mandated consolidation of insurance, leasing, real estate, and finance subsidiaries, generally: Increases leverage Decreases the reported return on assets Decreases the reported interest coverage of the parent firm’s debt Required consolidation of financial subsidiaries increases the probability of covenant violation for a parent firm with debt contracts employing restrictive covenants based on unconsolidated subsidiary reporting. Since contracts are costly to renegotiate, the stockholders of such parent firms face potential losses from the adoption of FAS 94. Firms with unconsolidated financial subsidiaries to be more likely to lobby against the standard than other firms. Some firms currently without unconsolidated financial subsidiaries to lobby against the proposal because it would restrict their accounting opportunity set, and the firm values the option to establish an unconsolidated financial subsidiary in the future.

15

However, firms’ incentives to lobby can be more subtle. Firms without unconsolidated financial subsidiaries have incentives to lobby for adoption of the FASB ED if adoption eliminates a valuable accounting option employed by their competitors. Firm with an unconsolidated subsidiary could have an incentive to lobby for passage of FAS 94, even though it imposes costs on itself, so long as the benefit from imposing costs on its competitors outweighs the self- imposed costs.

16

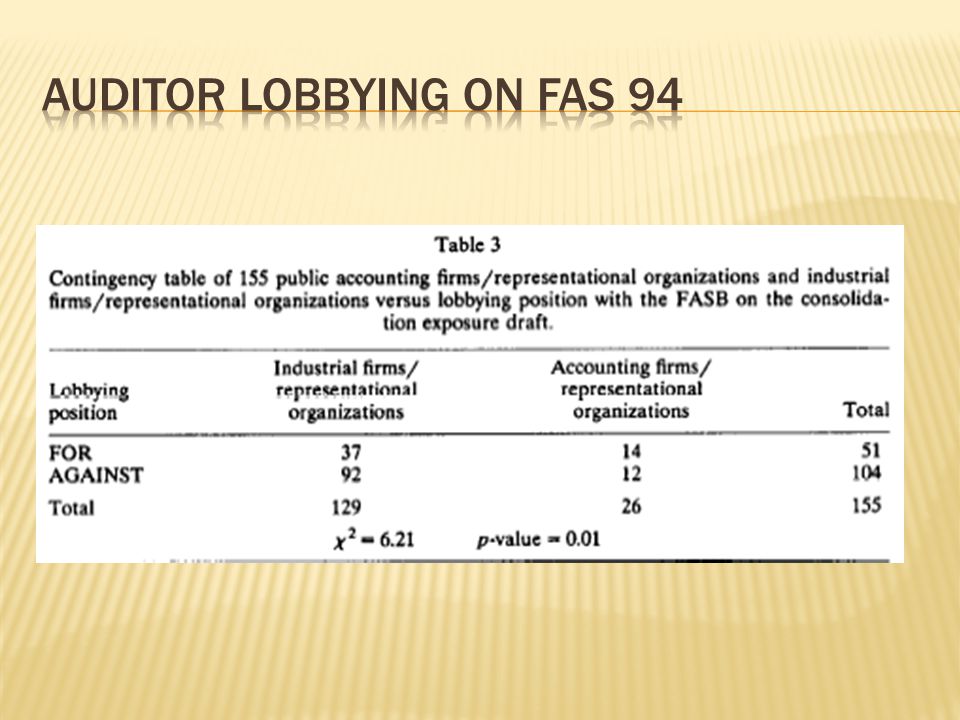

Of the 131 industrial corporations, we eliminate 8 firms that only submit comments, and 9 firms where we cannot determine the firm’s consolidation policy Firms with unconsolidated subsidiaries are more likely to lobby against the exposure draft and firms without unconsolidated subsidiaries are more likely to lobby for it.

20

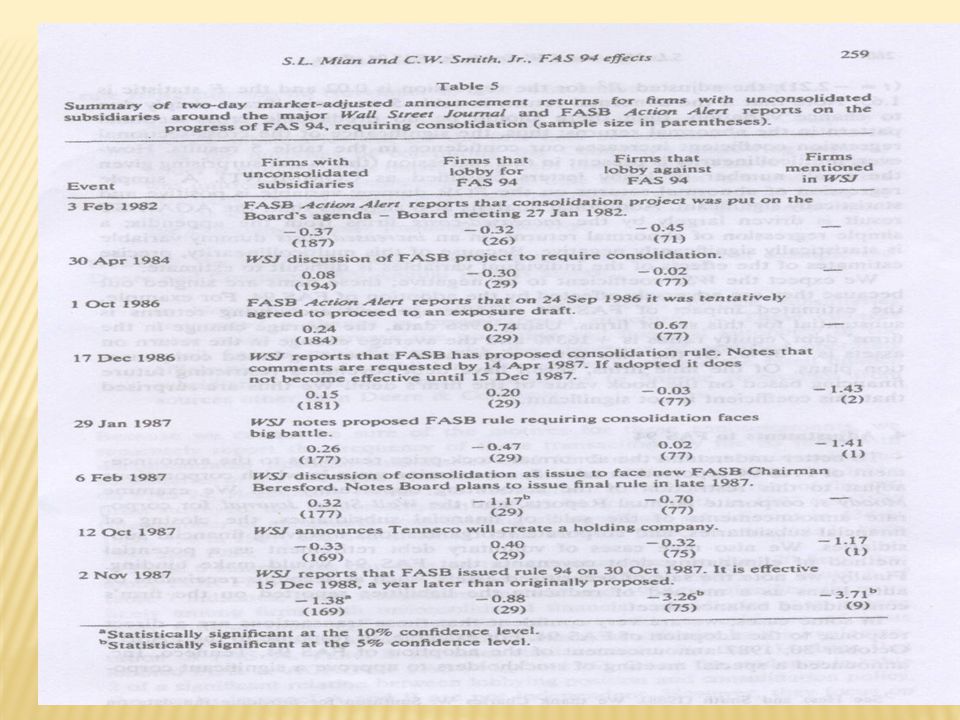

Estimated the value efffects associated with the adoption of FAS 94 : examine the abnormal return to the firm with unconsolidated financial subsidiaries around the time of the potentially relevant announchment (30 Oktober 1987, WJS 2 November 1987) The decision is preceded by six Wall Street Journal In table 5 : Various reaction for various subsets of firms Look at : Firms on CRSP that have unconsolidated finance The firms that lobby FOR and AGAINTS the FASB exposure draft The firms that mentioned specially in WJS articles

The decision is preceded by six Wall Street Journal In table 5 : Various reaction for various subsets of firms Look at : Firms on CRSP that have unconsolidated finance The firms that lobby FOR and AGAINTS the FASB exposure draft The firms that mentioned specially in WJS articles")

22

Note : identifiable stock price reaction is limited to Nov 1987 For 169 firms : abnormal return -1,38% t = - 1,69 (weak evidence) For the 75 firms againts FAS94: abnormal return - 3,26% t = -2,94 (the most significant) For the 29 firms lobby FOR : abnormal return – 0,88% This result consistent with preposition : That the firms with the most to lose from the adoption of FAS 94 incur the cost to lobby againts its passage

For the 75 firms againts FAS94: abnormal return - 3,26% t = -2,94 (the most significant) For the 29 firms lobby FOR : abnormal return – 0,88% This result consistent with preposition : That the firms with the most to lose from the adoption of FAS 94 incur the cost to lobby againts its passage")

23

To see whether the difference among the abnormal return is significant, use a regression where the Oct 30 and Nov 2 1987 AR, = -0.74 + 1.46 FOR, - 2.26 AGAINSTi -0.58 WSJj ( - 1.00) (0.57) (- 2.21) ( - 0.30) + 0.42 SIZE, + ej. (0.17) Explanation : Estimasi koefisien pada AGAINTS dummy secara statistik signifikan ( t = -2,21), adjusted R2 untuk regresi adalah 0.02 dan F statistic 1.65.

Explanation : Estimasi koefisien pada AGAINTS dummy secara statistik signifikan ( t = -2,21), adjusted R2 untuk regresi adalah 0.02 dan F statistic")

24

A simple regression of abnormal return on the FOR dummy variable is positive anda statisrically significant The AGAINTS result is driven largely by the increased cost and it is statistically significantly negative There are multicollinearity, so it is difficult to estimate Because the firms that mentioned in WJS are adverserly affected by FAS 94, coefficient is negative Using 1986 : average change in debt equity is + 163% and change in ROA is -39%, and of the nine firms, eight = accounting based compensation plan, and seven have debt covenants restricting future financing based on the book value of the firm’debt.

26

To better understand the reaction in table 5 : Examine ways in which corporation adjust to this restriction of the accounting apportunity set Examine Moody’s corporate annua report, and WJS for corporate announchement of the saleof financial subsidisries, the closing of financial subsidiaries, corporate reorganization Note cases of voluntary debt retirement as a potential method of eliminating debt covenants Note the sale of secirities asset (account receivable) as a method of reducing the liabilities reported on the firm’ consolidated balance sheet

as a method of reducing the liabilities reported on the firm’ consolidated balance sheet")

27

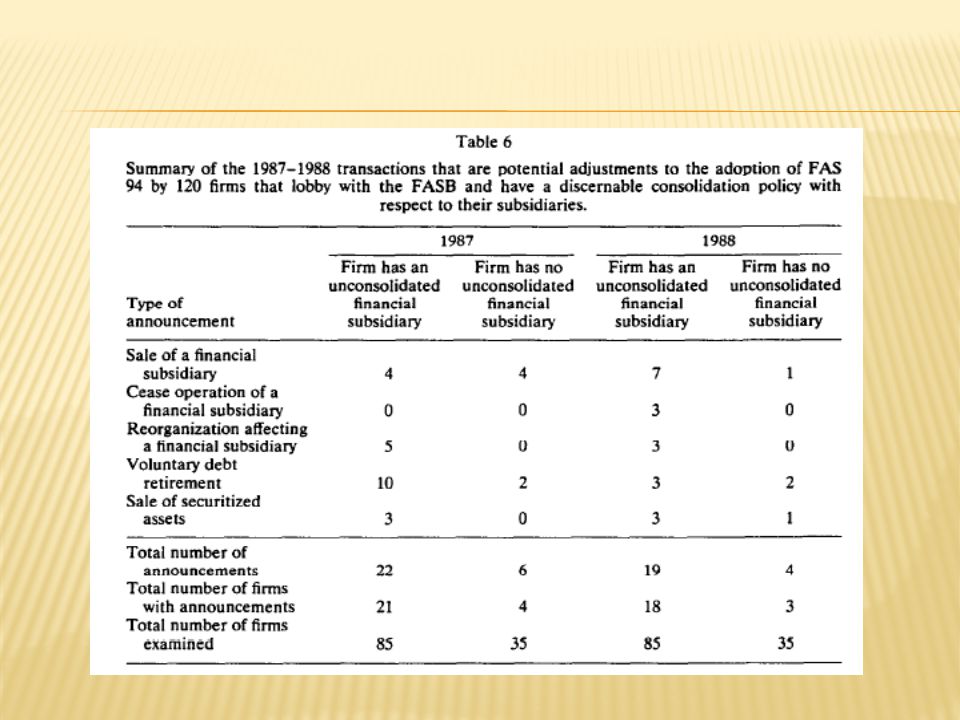

Because the motives of these annouchment cannot be sure : separAtely report the frequency of the transaction by the 85 firms with unconsolidated financial subsidiaries and 35 firms without unconsolidated subsidiaries of the 120 firms with discernables consolidatin poliies that lobby on FAS 94

28

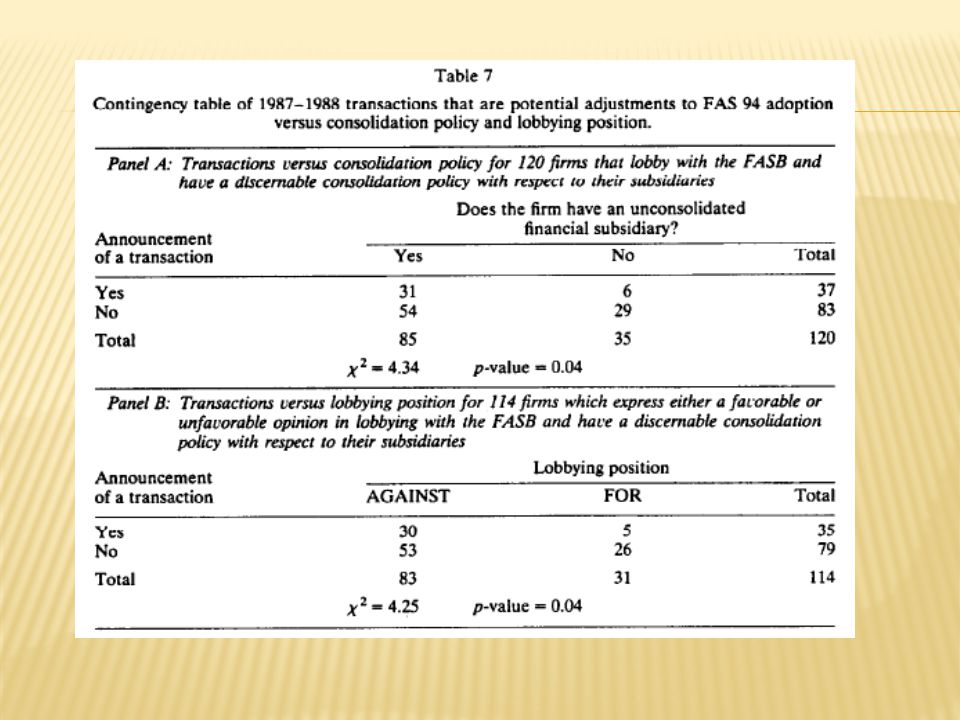

Table 6 summarizes data on these transaction for the 120 firms that lobby FOR FAS 94 Table 7 : panel A indicates these transaction in 1987 and 1988 are signifcantly more like among firms with unconsolidated financial subsidiaries than among firms without them. panel B indicates similar result for 114 firms that for lobby FOR or AGAINTS FAS 94

32

Data Financial Subsidiary yg dikonsolidasi : Financial Reporting (1975-1987) Penggunaan Financial Subsidiary di Canada lebih rendah daripada di US. FS before 1978 : perusahaan yang tidak dikonsolidasi sebesar 19% FS After 1978 : perusahaan yang tidak dikonsolidasi sebesar 44% Ketika teknik akuntansi yang memungkinkan tetap digunakan, perusahaan sebaiknya merubah jika net benefitnya positif

34

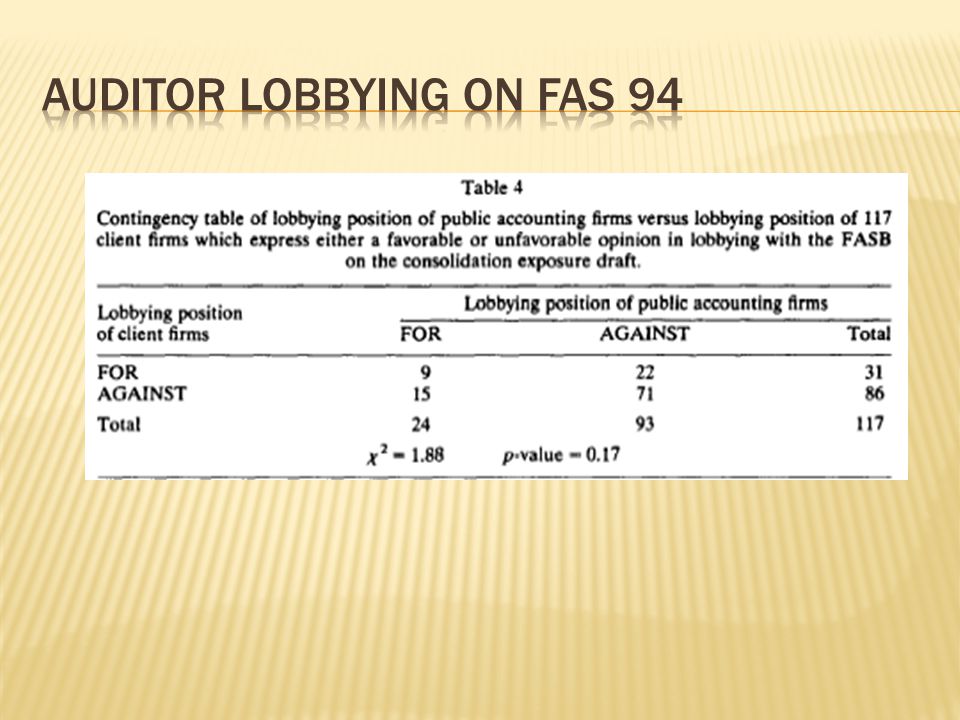

Perusahaan dengan FS tidak dikonsolidasi cenderung untuk melobi the Exposure Draft. Perusahaan akuntansi publik mendukung adanya exposure draft lebih sering dibandingkan perusahaan klien, dan sebaliknya untuk FASB, user jg melobi ED. Tidak menemukan hubungan yang signifikan antara klien dengan lobi auditor pada FAS 94. (-) antara harga saham terhadap pengumuman FAS 94, untuk perusahaan yang melobi ED. Pengujian tentang respon perusahaan terhadap keberadaan FAS 94 mengindikasikan bahwa frekuensi transaksi perusahaan dapat digunakan untuk mengurangi biaya pemenuhan FAS 94 yang lebih tinggi diantara perusahaan2 yang dengan subsidiary yang tidak dikonsolidasi.

antara harga saham terhadap pengumuman FAS 94, untuk perusahaan yang melobi ED. Pengujian tentang respon perusahaan terhadap keberadaan FAS 94 mengindikasikan bahwa frekuensi transaksi perusahaan dapat digunakan untuk mengurangi biaya pemenuhan FAS 94 yang lebih tinggi diantara perusahaan2 yang dengan subsidiary yang tidak dikonsolidasi..")

35

Penemuan MS menyarankan perusahaan2 untuk : 1. Menarik kontrak hutang jangka panjang yang sedang beredar. 2. Perubaan kegiatan korporasi untuk mengurangi implikasi perubahan akuntansi 3. Canada : ketika terjadi opportunity accounting yang disebabkan oleh adanya batasan yang lebih sedikit pada penggunaan yang dilaporkan yang tidak dikonsolidasi, perusahaan merubah laporan dari yang dikonsolidasi ke laporan yang tidak dikonsolidasi. Aspek pengujian : 1. Pengaruh FAS 94 pada persaingan 9 perusahaan dengan FS yang mendukung FOR ED. 2. Membuktikan analisa pengaruh perubahan terhadap efek wealth dan respon perusahaan terhadap perubahan standar akuntansi.

36

Regulagor/pemerintah akan lebih memahami bahwa pemilihan metode akuntansi oleh perusahaan telah memperhitungkan maximizing firm value Limitation : 1. Tidak memiliki teori yang menjelaskan mengapa perusahaan memanage beberapa aktiva perusahaannya, memisahkan beberapa aktivitas ke dalam beberapa divisi, menggunakan seluruh subsidiary yang dimiliki untuk melakukan aktivitas, melakukan kontrak dengan perusahaan eksternal melalui transaksi pasar untuk aktivitas lain 2. Insentif untuk melaporkan aktivitas subsidiary pada consolidated vs unconsolidated basis harus bersifat tentatif.

37

3. Data pada ukuran FS yang telah dikonsolidasi memungkinkan pengujian yang lebib powerful. 4. Data penelitian ini pada struktur kontrak perusahaan yang berasal dari Moody’s ketimbang dari kontrak perusahaan yang original.

Presentasi serupa

>")