Upload presentasi

Presentasi sedang didownload. Silahkan tunggu

1

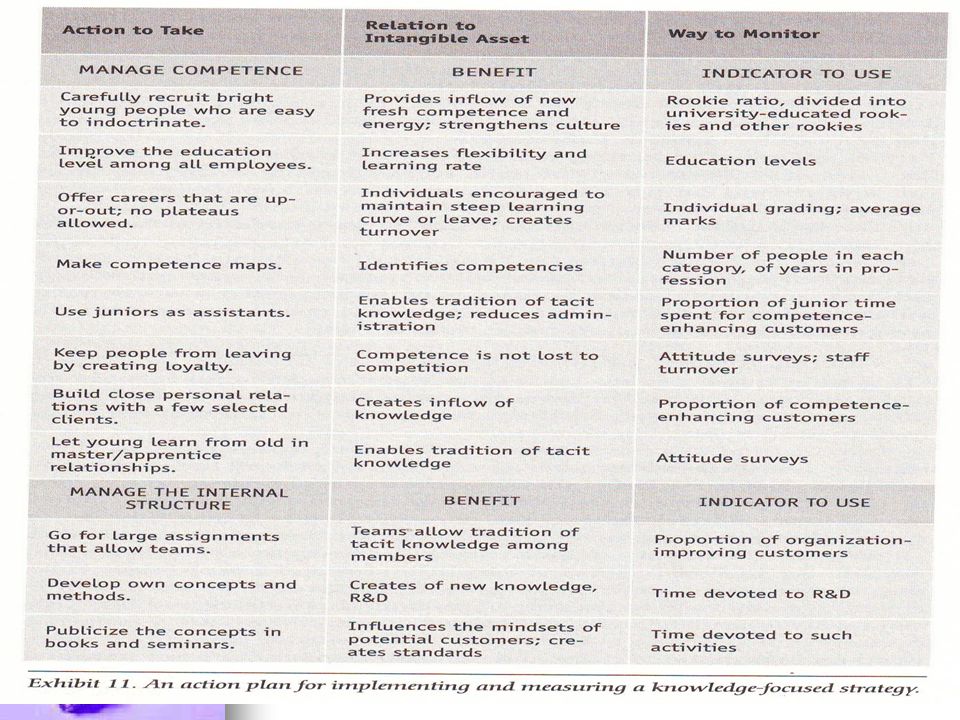

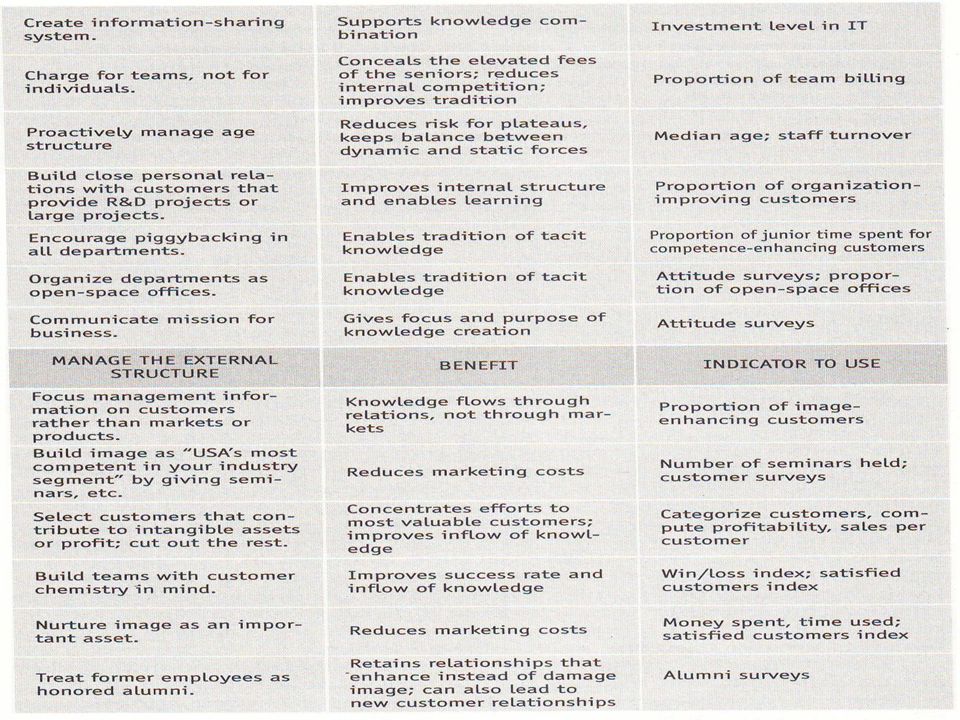

Implementing Systems for Measuring Intangible Assets Several case studies Reported the results publicly General guidelines for creating a measurement system

2

Public Reporting in Sweden & Denmark Swedia Pioner Annual reports Personnel statements Economics knowledge and competence of their workers Swedia Pioner Annual reports Personnel statements Economics knowledge and competence of their workers dibandingkan dibandingkan Computer consultants EDS and Cap Gemini Sogeti Berapa total pekerja Computer consultants EDS and Cap Gemini Sogeti Berapa total pekerjaContoh: WM-data WM-data Kategori-kategori External & internal structures and competence of personnel Growth/renewal, indicators of efficiency & indicators of stability Skandia AFS Skandia AFS Mempekerjakan seorang director of intellectual capital menemukan, memikirkan, merencanakan bagaimana menggambarkan intellectual capital

3

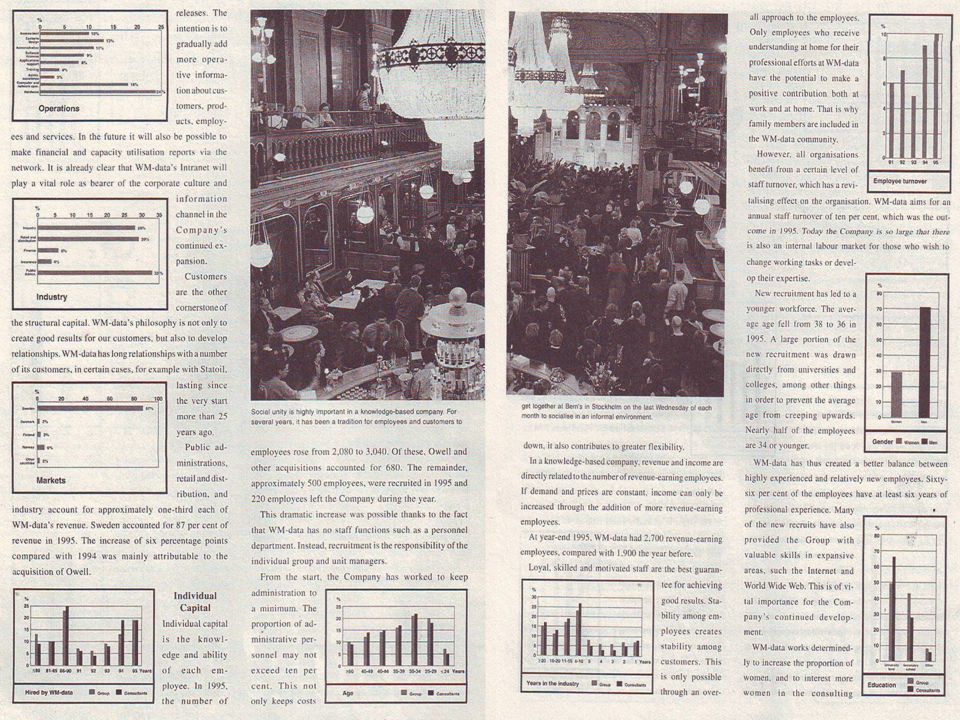

WM-Data’s 1995 Annual Reports Internal Structures External Structures Competence (5 pages Graphs & explanatory)

")

5

Skandia’s Process Measurement Financial Focus -Premium income - Result of operation Human Focus Empowerment index Process Focus -Processing time - Applications without error Customer Focus -Telephone accessibility - Policies without surrender Renewal Focus -R&D expense/administrative expense - IT expense/administrative expense - Competence development/employee Laporan & biaya administratif per karyawan Internal - Proporsi menejer dan menejer perempuan - Biaya training/pendidikan per karyawan Competence category -Indeks kepuasan karyawan -Ongkos marketing per langganan -Share of training hours External The Business Navigator Leif Edvinsson Intellectual Capital Director

6

Another Example… PLS-Consult Danish management consultancy PLS-Consult Danish management consultancy Menggambarkan dalam annual report bagaimana intangible assets pada tahun 1993-94 Menggambarkan dalam annual report bagaimana intangible assets pada tahun 1993-94 Membagi 3 tipe intangible structures: Membagi 3 tipe intangible structures: Customer capital (external), intellectual capital (competence) & organizational knowledge (internal). Customer capital (external), intellectual capital (competence) & organizational knowledge (internal). ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff

, intellectual capital (competence) & organizational knowledge (internal). ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff ffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffffff.")

7

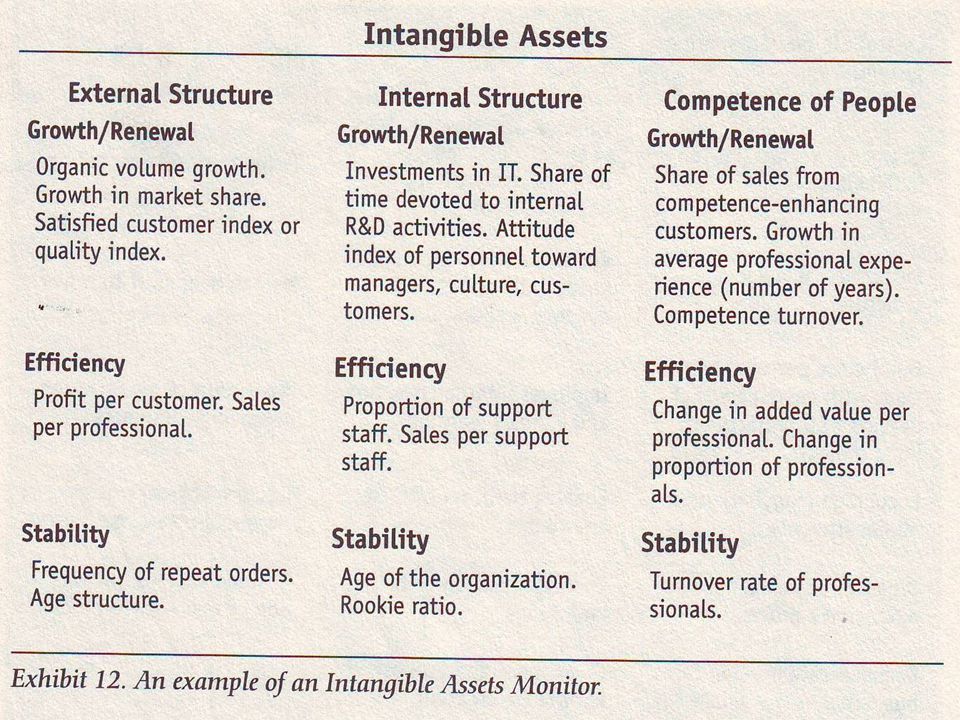

A Knowledge Audit of Celemi 1995 annual report (1 st ) Swedish company Develops & sells training tools Karl Erik Sveiby author Intangible assets : 1995 annual report (1 st ) Swedish company Develops & sells training tools Karl Erik Sveiby author Intangible assets : Our customer (external) Relation Our organization (internal) Struktural Our people (competence) Ability to act Visible revenue improve Tangible equity Invisible revenue improve Intangible assets How to monitor the intangible assets ? Image-enhancing customer Siapapun yang menaikkan Organization-enhancing customer Para profesional yang terlibat Competence-enhancing customer Siapapun yg bawa projek

8

Why isn’t intangibles reporting more widespread ? Banyak menejer merasa bahwa hal tersebut tidak ada gunanya. Lebih mengutamakan laporan keuangan, disebabkan tidak memiliki pengetahuan dalam penginterpretasian intangible assets. Banyak menejer merasa bahwa hal tersebut tidak ada gunanya. Lebih mengutamakan laporan keuangan, disebabkan tidak memiliki pengetahuan dalam penginterpretasian intangible assets. Memberikan dampak buruk kepada perusahaan. Memberikan dampak buruk kepada perusahaan. Tidak ada cara yang pasti dalam menulis laporan tersebut, key indicators sulit untuk ditemukan dan dikembangkan. Tidak ada cara yang pasti dalam menulis laporan tersebut, key indicators sulit untuk ditemukan dan dikembangkan.

9

Advices from Karl Erick Sveiby Advices from Karl Erick Sveiby Understand and act in the best way to face the confusing of changing in the modern business environment. Understand and act in the best way to face the confusing of changing in the modern business environment. To look consciously and understand the subtle differences between knowledge and information and have a feel for the strange markets we are encountering. We will be equipped to exploit the opportunities and circumvent the dangers that lie ahead. To look consciously and understand the subtle differences between knowledge and information and have a feel for the strange markets we are encountering. We will be equipped to exploit the opportunities and circumvent the dangers that lie ahead. Why is it necessary to look consciously ? Why is it necessary to look consciously ? Because so much of what we do is governed by attitudes and unconscious rules that obscure our vision. Why a knowledge perspective ? Why a knowledge perspective ? Because knowledge is the ultimate wellspring of unlimited resources and it is crucial for us to understand what knowledge is and what it is not. Information without knowledge is useless

13

Another advices… Knowledge Tacit Greater value Knowledge Tacit Greater value Information Explicit Do not despair if can make no sense of the indicators and are unable to assess the significance of changes in competence turnover, staff stability, customer, profitability and so on. Do not despair if can make no sense of the indicators and are unable to assess the significance of changes in competence turnover, staff stability, customer, profitability and so on.

14

Thank You Information without knowledge is useless

Presentasi serupa

>")

>")

Open Source vs Free Software oleh Razief Perucha F.A D3-Manajemen Informatika Jurusan Matematika – FMIPA Universitas.>")