Upload presentasi

1

Produktivitas Efektivitas Pemasaran

Prepared by Yudhi Herliansyah, Univ Mercubuana

2

Menggambarkan efektivitas dan implikasi perubahan dalam produktivitas.

Learning Objectives Slide 17-1 Menggambarkan efektivitas dan implikasi perubahan dalam produktivitas. Menghitung dan menginterpretasikan produktivitas parsial operasional dan finansial. Membedakan perubahan produktivitas, perub harga input dan perubahan output..

3

Learning Objectives Mengidentifikasi keuntungan dan kelemahan ukuran produktivitas pd perusahaan jasa dan organisasi nonprofit. Memisahkan sales volume variance dalam sales mix dan sales quantity variance. Menjelaskan bagaimana market size dan market share variances menimbulkan sales quantity variance.

4

Pengertian Produktivitas?

Productivity merupakan hubungan antara sesuatu yang diproduksi dan apa yang dihasilkan. Productivity = Output/Input

5

Benchmark Produktivitas

Kinerja tahun sebelumnya Kinerja Divisi lain dalam perusahaan Kinerja Kompetitor Ukuran yng di target oleh manajemen

6

Mengukur Produktivitas

Slide 17-5 Operational productivity adalah rasio unit output terhadap unit input, financial productivity adalah rasio output terhadap input dalam satuan mata uang,.

7

Mengukur Productivitas

Operational productivity adalah rasio unit output terhadap unit input, financial productivity adalah rasio output terhadap input dalam satuan mata uang,. Partial productivity adalah ukuran produktivitas yang hanya fokus pada hubungan antara input dan output yang dicapai.

8

Mengukur Productivitas

Ukuran produktivitas parsial: Produktivitas hasil bahan langsung, seperti output/units materials Produktivitas pekerja, seperti output per labor hours atau output per pekerja Produktivitas proses (atau activity), seperti output/machine hours atau output per kilowatt hours

, seperti output/machine hours atau output per kilowatt hours.")

9

Produktivitas Parsial =

10

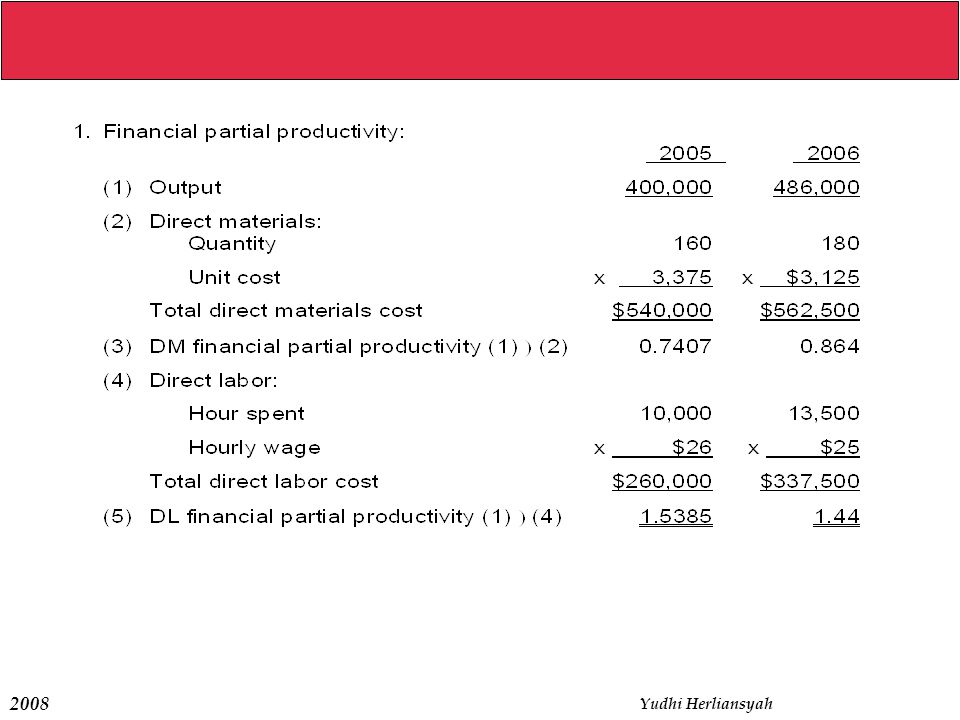

Data Operasi DB-2 tahun 2006 dan 2007 (dalam 000)

Mengukur Produktivitas Rizone Tool Company Data Operasi DB-2 tahun 2006 dan 2007 (dalam 000) Units DB-2 diproduksi dan dijual 4,000 4,800 Total Penjualan ($500 /unit) $2,000 $2,400 Direct materials (25,000 $24/pon.) ( Direct labor (4,000 $40 /jam) (4.000 $50/jam) Other operating costs Operating income $ $1,100

Units DB-2 diproduksi dan dijual 4,000 4,800. Total Penjualan ($500 /unit) $2,000 $2,400. Direct materials (25,000 $24/pon.) ( Direct labor (4,000 $40 /jam) (4.000 $50/jam) Other operating costs Operating income $ 940 $1,100.")

11

Produktivitas Parsial

Rizone Co Produktivitas Parsial Bahan baku dan Tenaga kerja untuk DB-2 Produktivitas Operasional Parsial Bahan Baku Langsung / = 0, / = 0,15 Tenaga Kerja Langsung / =1, / =1,20 Produktivitas Finansial Parsial Bahan Baku Langsung / = 0, / = 0,006 Tenaga Kerja Langsung / =0, / =0,024

12

Analisis Produktivitas Parsial Operasional

Produktivitas parsial bahan baku thn 2006 sebesar 0,16 unit output untuk setiap 1 pon input, sedangkan thn 2007 sebesar 0,15 terjadi penurunan produktivitas bahan baku sebesar 0,01 (6,25%) unit untuk setiap 1 pon input. Produktivitas parsial TKL thn 2006 sebesar 1 unit untuk setiap JKL sedangkan thn 2007 sebesar 1,2 unit untuk setiap JKL, terjadi peningkatan produktivitas sebesar 0,2 (20%).

unit untuk setiap 1 pon input. Produktivitas parsial TKL thn 2006 sebesar 1 unit untuk setiap JKL sedangkan thn 2007 sebesar 1,2 unit untuk setiap JKL, terjadi peningkatan produktivitas sebesar 0,2 (20%).")

13

Analisis Produktivitas Parsial Finansial

Produktivitas parsial bahan baku thn 2006 sebesar 0,0067 unit output untuk setiap 1 $ input, sedangkan thn 2007 sebesar 0,006 terjadi penurunan produktivitas bahan baku sebesar 0,007 (10%) unit untuk setiap 1 pon input. Produktivitas parsial TKL thn 2006 sebesar 0,025 unit untuk setiap $ TKL sedangkan thn 2007 sebesar 0,024 unit untuk setiap $ TKL, terjadi penurunan produktivitas sebesar 0,01 (4%).

unit untuk setiap 1 pon input. Produktivitas parsial TKL thn 2006 sebesar 0,025 unit untuk setiap $ TKL sedangkan thn 2007 sebesar 0,024 unit untuk setiap $ TKL, terjadi penurunan produktivitas sebesar 0,01 (4%).")

14

Produktivitas Operasional Parsial

EPT Co Dampak perubahan Produktivitas Parsial Bahan baku dan TKL prod D82 Sumberdaya Input (1) Output 2007 (2) Produktivitas Operasional Parsial 2006 (3) =(1 : 2) Output 2007 Pd produktivitas 2006 (4) Input yg digunakan dl thn 2007 (5)=(3-4) Penghematan atau (Kerugian) dl Input Bahan Baku Langsung 4.800 0,16 30.000 32.000 (2.000) TKL 1,00 4.000 800

Output (2) Produktivitas. Operasional. Parsial (3) =(1 : 2) Output Pd produktivitas (4) Input yg. digunakan dl thn (5)=(3-4) Penghematan. atau (Kerugian) dl Input. Bahan. Baku. Langsung , (2.000) TKL. 1,")

15

Tabel diatas: menunjukkan bahwa penurunan Produktivitas bahan baku pada tahun 2007 disebabkan terdapat peningkatan penggunaan input sebesar 2000 unit. Menunjukkan bahwa peningkatan produktivitas TKL disebabkan penghematan sebesar 800 JKL.

16

Produktivitas Parsial Financial

Decomposition of Financial Partial Productively 17 Slide 17-8 Managing Productivity and Marketing Effectiveness Rizone Tool Company Produktivitas Parsial Financial (A) (B) (C) (D) Kerangka Output: 20x7 20x7 20x7 20x6 Productivity: 20x7 20x6 20x6 20x6 Input costs: 20x7 20x7 20x6 20x6 Perubahan Perubahan harga Perubahan Produktivitas Input Output

(B) (C) (D) Kerangka. Output: 20x7 20x7 20x7 20x6. Productivity: 20x7 20x6 20x6 20x6. Input costs: 20x7 20x7 20x6 20x6. Perubahan Perubahan harga Perubahan. Produktivitas Input Output.")

17

Decomposition of Financial Partial Productively

output 2007 pd output 2007 pd Hasil Operasi produktivitas Produktivitas Hasil Opr Aktual dgn By input dan By input Aktual 06 Output units: 4,800 4,800 4,800 4,000 unit Input dan costs: DM: 32,000 x $25= 30,000 x $25 = 30,000 x $24 = 25,000 x $24 = $800,000 $750,000 $720,000 $600,000 DL: 4,000 x $50 = 4,800 x $50 = 4,800 x $40 = 4,000 x $40 = 200, , , ,000 Totals $1,000,000 $990,000 $912,000 $760,000

18

Decomposition of Financial Partial Productively

Operasi Operasi 2006 Output 2007/ output 2007/(input output 2007/(input output 06 (input 2006 x utk output x utk output /(input 06 by input07) By input x By input by inpt 06 DM : / / / / = 0, = 0, = 0, =0,006667 DL : / / / / = 0, = 0, = 0, =0,02500 Perub Produktivitas Perub Harga input Perub Output DM : ,006-0,0064 =0,0004 U 0,0064-0,006667= 0, U , ,006667=0 DL : ,024-0,020 = 0,004 F 0,020-0,025 =0,005 U ,025-0,025 = 0

By input 2007 x By input 2006 by inpt 06. DM : 4.800/ / / / = 0,006 = 0,0064 = 0, =0, DL : 4.800/ / / / = 0,024 = 0,0200 = 0, =0, Perub Produktivitas Perub Harga input Perub Output. DM : 0,006-0,0064 =0,0004 U 0,0064-0,006667= 0, U 0, ,006667=0. DL : 0,024-0,020 = 0,004 F 0,020-0,025 =0,005 U 0,025-0,025 = 0.")

19

Perubahan Produktivitas dari 2006

Perub Produktivitas Perub Harga input Perub Output Total Perub DM ,0004 U ,00267 U = 0, U DL , ,005 U = 0,001 U Perubahan sbg %tase Produktivitas dari 2006 DM % U % U = % U DL % F % U = 4% U

20

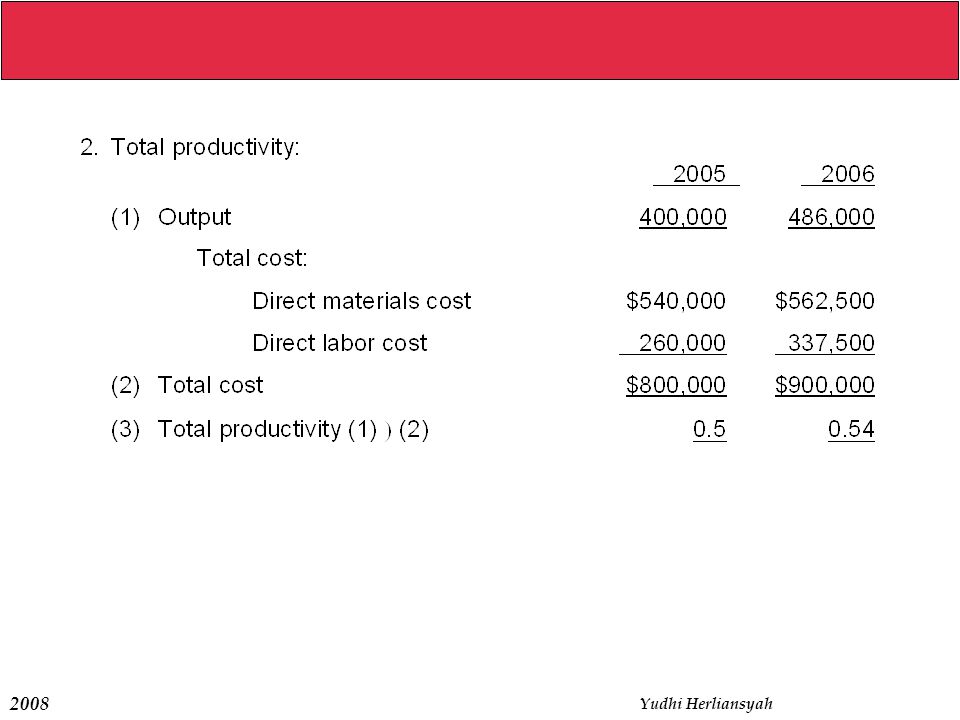

ProduktivitasTotal dapat dihitung sbb:

21

Data Operasi DB-2 tahun 2006 dan 2007

Produktivitas Total Rizone Tool Company Data Operasi DB-2 tahun 2006 dan 2007 1. Produktivitas Total dalam Unit a. Total unit yg diproduksi , ,800 b. Total Biaya prod variabel yg terjadi $760, $ c. Produktivitas Total= a/b , ,0048 d. Penurunan Produktivitas tahun 2007: 0, (8,8%) 2. Produktivitas Total dl $ Penjualan a. Total Penjualan $ $ b. Total By prod var $760, $ c. Produktivitas Total= a/b $ 2, $2,40 d. Penurunan Produktivitas tahun 2007= 0,2316 (8,8%)

2. Produktivitas Total dl $ Penjualan. a. Total Penjualan $ $ b. Total By prod var $760,000 $ c. Produktivitas Total= a/b $ 2,6316 $2,40. d. Penurunan Produktivitas tahun 2007= 0,2316 (8,8%)")

22

Kerjakan hal

25

Managing Marketing Effectiveness

Pemasaran yg efektif membuat perusahaan mampu: achieving budgeted operating income attaining budgeted market share adapting to change in the market

26

17 Sales Variances and Its Components Sales Variance

Slide 17-15 Managing Productivity and Marketing Effectiveness Sales Variance

27

Sales Variances and Its Components

Sales Price Variance Sales Volume Variance

28

Sales Variances and Its Components

Sales Price Variance Sales Volume Variance Sales Quantity Variance Sales Mix Variance

29

Sales Variances and Its Components

Sales Price Variance Sales Volume Variance Sales Quantity Variance Sales Mix Variance Market Size Variance Market Share Variance

30

Sales Mix Variance - Schmidt Machinery

Sales mix Actual sales Budget sales Actual total Budgeted unit variance for = mix percentage - mix percentage x units of all x contribution margin a product for the product for the product products sold of the product

31

Sales Mix Variance - Schmidt Machinery

Sales mix Actual sales Budget sales Actual total Budgeted unit variance for = mix percentage - mix percentage x units of all x contribution margin a product for the product for the product products sold of the product Sales mix variance = ( ) x 4,000 units x $350 = $77,000 U of XV-1

x 4,000 units x $350 = $77,000 U. of XV-1.")

32

Sales Mix Variance - Schmidt Machinery

Sales mix Actual sales Budget sales Actual total Budgeted unit variance for = mix percentage - mix percentage x units of all x contribution margin a product for the product for the product products sold of the product Sales mix variance = ( ) x 4,000 units x $350 = $77,000 U of XV-1 Sales mix variance = ( ) x 4,000 units x $280 = $61,600 F of FB-33

x 4,000 units x $350 = $77,000 U. of XV-1. Sales mix. variance = ( ) x 4,000 units x $280 = $61,600 F. of FB-33.")

33

Total sales mix variance - $77,000 U + $61,600 F = $15,400 U

Sales Mix Variance - Schmidt Machinery Sales mix Actual sales Budget sales Actual total Budgeted unit variance for = mix percentage - mix percentage x units of all x contribution margin a product for the product for the product products sold of the product Sales mix variance = ( ) x 4,000 units x $350 = $77,000 U of XV-1 Sales mix variance = ( ) x 4,000 units x $280 = $61,600 F of FB-33 Total sales mix variance - $77,000 U + $61,600 F = $15,400 U

x 4,000 units x $350 = $77,000 U. of XV-1. Sales mix. variance = ( ) x 4,000 units x $280 = $61,600 F. of FB-33. Total sales mix variance - $77,000 U + $61,600 F = $15,400 U.")

34

Sales Quantity Variance - Schmidt Machinery

Sales quantity Actual total Budgeted total Budgeted sales Budgeted contri- variance for = units of all sales units of x mix percentage x bution margin per a product products sold all products of the product unit of the product

35

Sales Quantity Variance - Schmidt Machinery

Sales quantity Actual total Budgeted total Budgeted sales Budgeted contri- variance for = units of all sales units of x mix percentage x bution margin per a product products sold all products of the product unit of the product Sales quantity variance for = (5, ,000) x 0.25 x $350 = $ 87,500 favorable XV-1

x 0.25 x $350 = $ 87,500 favorable. XV-1.")

36

Sales Quantity Variance - Schmidt Machinery

Sales quantity Actual total Budgeted total Budgeted sales Budgeted contri- variance for = units of all sales units of x mix percentage x bution margin per a product products sold all products of the product unit of the product Sales quantity variance for = (5, ,000) x 0.25 x $350 = $ 87,500 favorable XV-1 Sales quantity variance for = (5, ,000) x 0.75 x $280 = 210,000 favorable FB-33

x 0.25 x $350 = $ 87,500 favorable. XV-1. Sales quantity. variance for = (5, ,000) x 0.75 x $280 = 210,000 favorable. FB-33.")

37

Sales Quantity Variance - Schmidt Machinery

Sales quantity Actual total Budgeted total Budgeted sales Budgeted contri- variance for = units of all sales units of x mix percentage x bution margin per a product products sold all products of the product unit of the product Sales quantity variance for = (5, ,000) x 0.25 x $350 = $ 87,500 favorable XV-1 Sales quantity variance for = (5, ,000) x 0.75 x $280 = 210,000 favorable FB-33 Total $297,500 favorable

x 0.25 x $350 = $ 87,500 favorable. XV-1. Sales quantity. variance for = (5, ,000) x 0.75 x $280 = 210,000 favorable. FB-33. Total $297,500 favorable.")

38

Schmidt Machinery Company Further Analysis of Sale Quantity Variance

Sales Quantity Variance - Schmidt Machinery Schmidt Machinery Company Further Analysis of Sale Quantity Variance For December 20x2 Product Sales Mix Budgeted Mix Margin per Unit Total Contribution Margin XV x 0.25 = 1250 $350 $350 x 1,250 = $ 437,500 FB x 0.75 = 3,750 $280 $280 x 3,750 = $1,050,000 Total contribution margin of the total units sold at the budgeted mix $1,487,500 Budgeted fixed expenses ,000 Operating income from the sale of the total actual units at the budgeted mix $ 887,500 Operating income at the master budget ,000 Sales quantity variance $ 297,500

39

Sales Mix Variance - Schmidt Machinery

Flexible Budget with Actual Sales Mix Flexible Budget with Budgeted Sales Mix Total actual units of all products sold x Actual sales mix x Budgeted contribution margin Total actual units of all products sold x Budgeted sales mix x Budgeted contribution margin per unit XV-1

40

Sales Mix Variance - Schmidt Machinery

Flexible Budget with Actual Sales Mix Flexible Budget with Budgeted Sales Mix 5,000 x 0.32 x $350 = $560,000 5,000 x .025 x $350 = $437,500 XV-1 Sales mix variance, $122,500 F

41

Sales Quantity Variance - Schmidt Machinery

Flexible Budget with Budgeted Sales Mix Master Budget 5,000 x .025 x $350 = $437,500 Total budgeted units of sales for all products x Budgeted sales mix x Budgeted C/M per unit XV-1

42

Sales quantity variance, $87,500 F

Sales Quantity Variance - Schmidt Machinery Flexible Budget with Budgeted Sales Mix Master Budget 5,000 x .025 x $350 = $437,500 4,000 x 0.25 x $350 = $350,000 XV-1 Sales quantity variance, $87,500 F

43

Sales quantity variance, $210,000 F

Sales Volume Variance - Schmidt Machinery Flexible Budget with Actual Sales Mix Master Budget 5,000 x 0.32 x $350 = $560,000 4,000 x 0.25 x $350 = $350,000 XV-1 Sales quantity variance, $210,000 F

44

Market Size and Market Share Variances

Market size variance Mengukur pengaruh perubahan ukuran pasar thd hasil operasi termasuk terhadap total margin kontribusi dan laba operasi. Market share variance menilai pengaruh perubahan proporsi pasar perusahaan dari total pasar thd hasil operasi perusahaan termasuk terhadap total margin kontribusi dan laba operasi perusahaan

45

Market Size Variance - Schmidt Machinery

Market Actual total Budgeted Budgeted Weighted size = units of the - total units of x market x average variance market the market share budgeted c/m per unit

46

Market Size Variance - Schmidt Machinery

Market Actual total Budgeted Budgeted Weighted size = units of the - total units of x market x average variance market the market share budgeted c/m per unit Market size = (31, ,000) x 0.1 x $ = $260, U variance

x 0.1 x $ = $260, U. variance.")

47

Market Share Variance - Schmidt Machinery

Market Actual Budgeted Actual total Weighted share = market market x units of the x average variance share share industry budgeted c/m per unit

48

Market Share Variance - Schmidt Machinery

Market Actual Budgeted Actual total Weighted share = market market x units of the x average variance share share industry budgeted c/m per unit Market share = ( ) x 31,250 x $ = $557, F variance

x 31,250 x $ = $557, F. variance.")

49

The End

Kerangka kerja untuk melakukan analisis selisih yang terjadi menggunakan ide-ide sebagai.>")

ANALYSIS>")

>")