Activity – Based Management 31/10/2009Akuntansi Manajemen Lanjutan

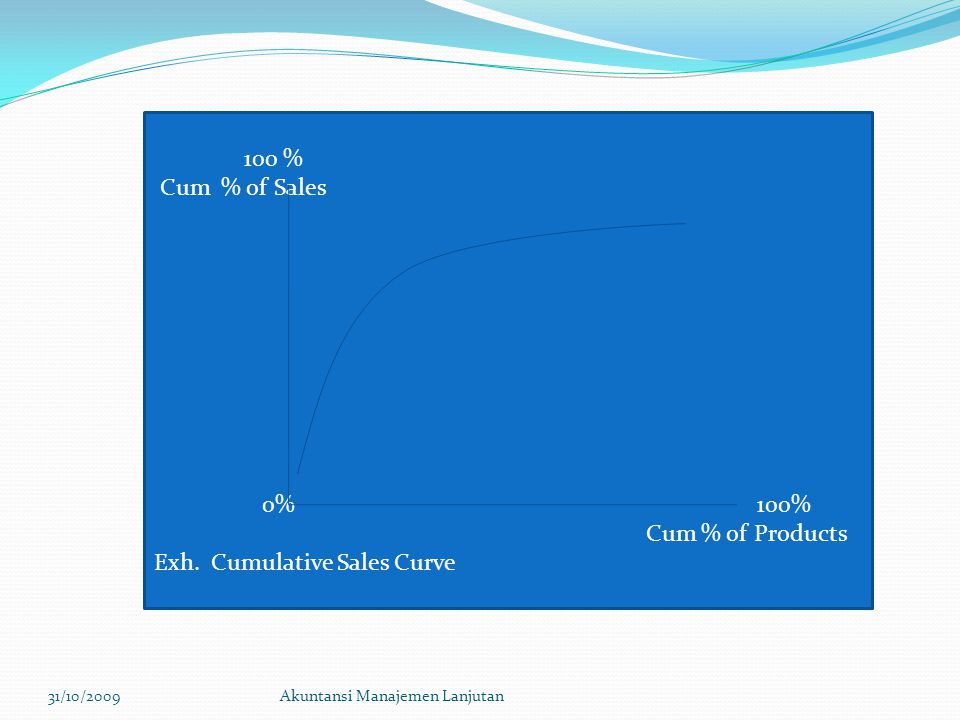

31/10/2009Akuntansi Manajemen Lanjutan 100 % Cum % of Sales 0% 100% Cum % of Products Exh. Cumulative Sales Curve

LINGKUP SISTEM KEPUTUSAN MANAJEMEN BERDASARKAN ABC 31/10/2009Akuntansi Manajemen Lanjutan PRODUCT PROFITABILITAS CUSTOMER VALUE MANAJER STRATEGI PERUSAHAAN INFORMASI BERDASARKAN AKTIVITAS TEKNIK-TEKNIK PROSES

Reprice products Substitute products Redesign products Improve processes and operations strategy Technology investment Eliminate products 31/10/2009Akuntansi Manajemen Lanjutan

Product Markets 31/10/2009Akuntansi Manajemen Lanjutan

31/10/2009Akuntansi Manajemen Lanjutan Pricing to improve the profitability : Redesigning Substituting Eliminating Improving processes

Model M. Porter Cara Menentukan Strategi 31/10/2009Akuntansi Manajemen Lanjutan Competitive Scope Nasional Lokal Diferensiasi Biaya RendahCompetitive Advantage Strategi Diferensiasi Strategi Kepemimpinan Biaya Strategi Fokus Diferensiasi Strategi Fokus Biaya

ABC Costing for a New Order Exp. The Glenn Company, a manufacturer of electromechanical components. 31/10/2009Akuntansi Manajemen Lanjutan ACTIVITYACTIVITY COST DRIVER RATE Direct labor processing$50/hour Material processing$60/hour Purchase and receive components$150/purchase order Schedule production orders and$200/production run perform list item inspection Set up machine$80/set up hour Process customer order$100/customer order Perform engineering design and support$75/engineering hour

The product with the following characteristics : 31/10/2009Akuntansi Manajemen Lanjutan Material cost pe unit$12.40 Direct labor time per unit produced0.6 hours Machine hours per unit produced0.8hours Number of component purchases10 Number of production runs6 Average setup time per production run3 hours Number of shipments1 Engineering design and process time20hours

The cost buildup for the product is : (100 units) 31/10/2009Akuntansi Manajemen Lanjutan Material (12.4*100)$1,200 Direct labor (0.6*50*100)3,000 Machining (0.8*60*100)4,800 Unit - level expenses$9,040 Acquiring material (10*150)1,500 Production runs (6*200)1,200 Setup machines (6*3*80)1,440 Process customer order (1*100)100 Batch - level expenses$4,240 Engineering support (20*75)1,500 Product - sustaining expenses$1,500 Total product expenses$14,780

The cost buildup for the product is : (1000 units) 31/10/2009Akuntansi Manajemen Lanjutan Material (12.4*1000)$12,000 Direct labor (0.6*50*1000)30,000 Machining (0.8*60*1000)48,000 Unit - level expenses$90,400 Acquiring material (10*150)1,500 Production runs (6*200)1,200 Setup machines (6*3*80)1,440 Process customer order (1*100)100 Batch - level expenses$4,240 Engineering support (20*75)1,500 Product - sustaining expenses$1,500 Total product expenses$96,140

USING ABC FOR ANALYZING CUSTOMER PROFITABILITY 31/10/2009Akuntansi Manajemen Lanjutan ProfitTypes of CustomersCustomer that are Hi above the cost - plus Passive : Costly to service,diagonal are more Product is crucialbut pay top dollarprofitable good supplier Net Margin Realized Aggressive: Price-sensitive and fewLeverage their baying power special demandsLow price and lots of customized service and features Low Hi Cost to ServeLosser Ex. Option for Managing Customers

31/10/2009Akuntansi Manajemen Lanjutan