Upload presentasi

Presentasi sedang didownload. Silahkan tunggu

1

DELEGATION AND INCENTIVE COMPENSATION BY: V ENKY N AGAR ( THE A CCOUNTING R EVIEW ; A PR 2002;77; 2) Kelompok VII: Dhani Pradipta Paramita Fazli Syam BZ Herni Kurniawati )

Kelompok VII: Dhani Pradipta Paramita Fazli Syam BZ Herni Kurniawati )")

2

O UTLINE Introduction Research Questions Research Goals Theory Research Method Result Conclusions

3

I NTRODUCTION The reason of top management (1) seberapa besar otoritas yang akan didelegasikan kepada manajer tingkat bawah (2) bagaimana mendesain kompensasi insentif untuk meyakinkan bahwa manajer ini tidak menyalahgunakan wewenang/otoritas yang diberikan (Milgrom dan Roberts, 1992, Stiglitz, 1994,; Brickley et al. 1996).

..")

4

DELEGATION AND INCENTIVE COMPENSATION Bukti empiris yang pertama kali ditemukan Hubungan dua pilihan desain organisasional Top Management (1) Penyerahan wewenang/otoritas kepada manajer tingkat bawah, dan (2) Ketentuan kompensasi insentif untuk memastikan agar para manajer tingkat bawah tersebut tidak menyalahgunakan wewenang/otoritas yg telah diberikan.

Penyerahan wewenang/otoritas kepada manajer tingkat bawah, dan (2) Ketentuan kompensasi insentif untuk memastikan agar para manajer tingkat bawah tersebut tidak menyalahgunakan wewenang/otoritas yg telah diberikan.")

5

C ONTINU ’ D Prior researchs Melumad dan Reichelstein (1987): The joint nature of the firm’s delegation and incentive compensation choices Horngren et al. (2000, 1995 – 1996): Responsibility Accounting Holthausen et al. dan Bushman et al. (1995): Not control authority of delegated to the managers Baiman et al. (1995): Not control authority of delegated to the managers

: Responsibility Accounting Holthausen et al. dan Bushman et al. (1995): Not control authority of delegated to the managers Baiman et al. (1995): Not control authority of delegated to the managers.")

6

The results of Baiman’s research A positive association between CEO expertise and divisonal manager incentive compensation The greater CEO division expertise is associated wit less powerful incentive compensation for divisonal managers C ONTINU ’ D

7

R ESEARCH Q UESTION Bagaimanakah perancangan sistem pendelegasian dan kompensasi insentif yang disusun oleh top management terhadap manajemen yang lebih rendah?

8

Research Goals Menguji secara empiris pilihan kompensasi insentif dan delegasi untuk manajer cabang pada bank-bank retail Menguji hubungan empiris antara delegasi dan kompensasi insentif pada manajer cabang di bank retail

9

THEORY ♠ Melumad dan Reichelstein (1987), Kirby (1987), Jensen dan Meckling (1992), Bushman et al. (2000), dan Prendergast (2000) ♠ Prendergast (2000) ♠ Kreps (1990): Teori principal-agents dan model simultan Tingkat delegasi = f(Tingkat kompensasi insentif, lingkungan operasional perusahaan) Tingkat kompensasi insentif = f(Tingkat delegasi, lingkungan operasional perusahaan ♠ Ittner et al. (2001) : branch earnings ♠ Ittner dan Larcker (1998) : branch earnings dalam timelier manner

, dan Prendergast (2000) ♠ Prendergast (2000) ♠ Kreps (1990): Teori principal-agents dan model simultan Tingkat delegasi = f(Tingkat kompensasi insentif, lingkungan operasional perusahaan) Tingkat kompensasi insentif = f(Tingkat delegasi, lingkungan operasional perusahaan ♠ Ittner et al. (2001) : branch earnings ♠ Ittner dan Larcker (1998) : branch earnings dalam timelier manner.")

10

R ESEARCH M ETHOD 1. Data 2. Variable definition and variable measurement 3. Spesification of Model

11

C ONT ’ D 1. Data Diperoleh dari 2 sumber Survey bank retail Wharton Financial Institutions Center (WFIC) tahun 1994 Bank call report yang disimpan oleh Federal Deposit Insurance Corporation (FDIC).

tahun 1994 Bank call report yang disimpan oleh Federal Deposit Insurance Corporation (FDIC)..")

12

C ONT ’ D Survey bank retail Wharton Financial Institutions Center (WFIC) tahun 1994 Responden (eksekutif senior bank retail dan manajer cabang dari kepala kantor cabang) Ada 2 tahap : 1. Tim riset 70 perusahaan pemilik bank terbesar di US 47 perusahaan pemilik bank sampel sebanyak 64 bank 2. Tim riset perusahaan besar lainnya (256 bank holding companies) 64 perusahaan berpartisipasi sampel sebanyak 71 bank Jumlah sampel 135 bank

64 perusahaan berpartisipasi sampel sebanyak 71 bank Jumlah sampel 135 bank.")

13

C ONT ’ D Bank call report yang disimpan oleh Federal Deposit Insurance Corporation (FDIC) Neraca kuartalan, Laporan Laba Rugi, dan data keuangan lain pengecekan antara WFIC dan call report sebanyak 100 bank

Neraca kuartalan, Laporan Laba Rugi, dan data keuangan lain pengecekan antara WFIC dan call report sebanyak 100 bank")

14

VARIABLE DEFINITIONS

15

Survey Questions: 1.Discretion available to the branch manager in hiring tellers. 2.Discretion available to the branch manager in awarding promotions in the branch. 3.Discretion available to the branch manager in determining the hours the branch is open. 4.Discretion available to the branch manager in changing the process for selling new investment products. DELEGATE : The standardized aggregated sum of the branch manager’s authority in hiring, promoting, setting hours, and changing selling processes. DELEGATION FACTOR ANALYSIS SURVEY ITEMS

16

INCENTIVE COMPENSATION INCENTIVE: The proportion of the typical branch manager’s pay that is bonus-based WFIC INCENTIVE a categorical measure of whether the typical magnitude of the bonus lies within certain ranges, e.g., “1-6 percent of total pay”, or “7-10 percent”, etc., with the highest category beign “25 percent and above.” Since the WFIC survey question does not specify whether respondents should indicate potential or actual compensation, INCENTIVE may be a noisy indicator of performance compensation

17

FIRM’S OPERATING ENVIRONMENT (1) Three measures: Firm growth Volatility of earnings The firm’s strategic emphasis on innovation FIRM GROWTH Firm growth insured deposit growth. Measure growth from June 1994 – June 1995 to cover grwoth prior to December 1994 and anticipated future growth. GROWTH: The growth in insured deposits from June 1994 – June 1995 VOLATILITY OF EARNINGS Ittner et al. Because earnings comprise one of the most important performance measures for branch manager ue the volatility of earnings as a measure of volatility facing the branch manager. STDROA : Standard deviation of the bank’s net income scaled by assets from 1990-1994

18

FIRM’S OPERATING ENVIRONMENT (2) THE FIRM’S STRATEGIC EMPHASIS ON INNOVATION Innovation WFIC survey item on the firm’s strategic emphasis on innovation. INNOV : The extent to which the firm emphasizes innovation in the design and delivery pof products and services Firm size is associated with all critical organizational design choices control for the bank’s retail division size, using the lof of deposits. SIZE: The log of insured deposits

19

MODEL SPECIFICATION

20

Exogenous Variable for the Delegation Equation Exogenous variable affecting delegation the number of acquisitions. Acquisitions should affect incentive compensation only indirectly, throught the delegation effect. To allow for both past and anticipated acquisitions count the number of acquisitions the bank made from June 1994 – June 1995. ACQUIRE: The sum of the number of azquisitions the bank made from June 1994 throught June 1995, adjusted for size. Following the FDIC categorization, if a particular acquisition increases assets by less than 25 percent, then it is counted as 1; otherwise, it is counted as 2. I then sum all the bank’s acquisitions over the June 1994 – June 1995 period.

21

EMPIRICAL MODEL for the delegation choice INCENTIVE should have a negative coefficient as stronger incentives imply a higher risk premium. I expected the next three coeficients on the right side of the equation to be positive, as greater growth, volatility, and innovation require more delegation. I do not predict the direction pf the size effect, as firm size can proxy for several constructs. I expect the acusition coefficient to be negative, as acquisitions require more centralized decision making.

22

Exogenous Variable for the Incentive Compensation Equation Exogenous variable for the incentive Equation proxies for the branch manager’s risk aversion. Measure the branch manager’s risk aversion by his eduaction and experience with other banks. EDUCATE: Level of the bracnh manager’s education EXPERIENCE: A binary variable that measures whether the bank manager has worked for other banks.

23

INCENTIVE COMPENSATION EQUATION DELEGATE should have a positive coefficient, as branch managers who exercise greater authority should receive more incentive compensation. The next three variables should have negative coefficients. I do not predict the sign pf the SIZE coefficient, because firm size can proxy for several constructs. EDUCATE and EXPERIENCE should have positive coefficients, as they for risk tolerance, which should be positively relatef to the extent of incentive compensation.

24

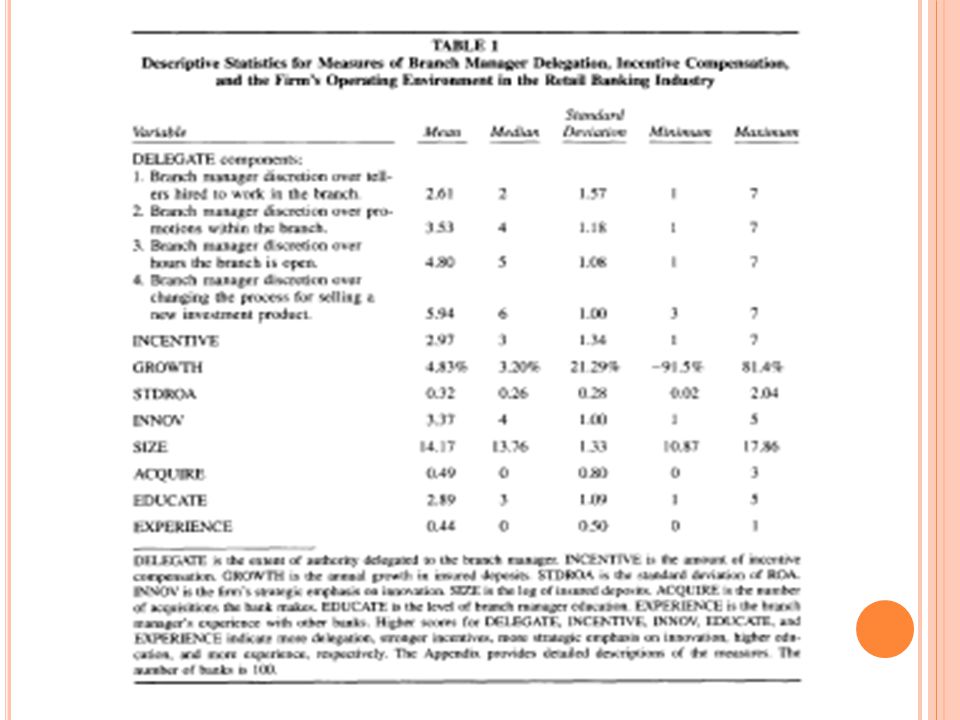

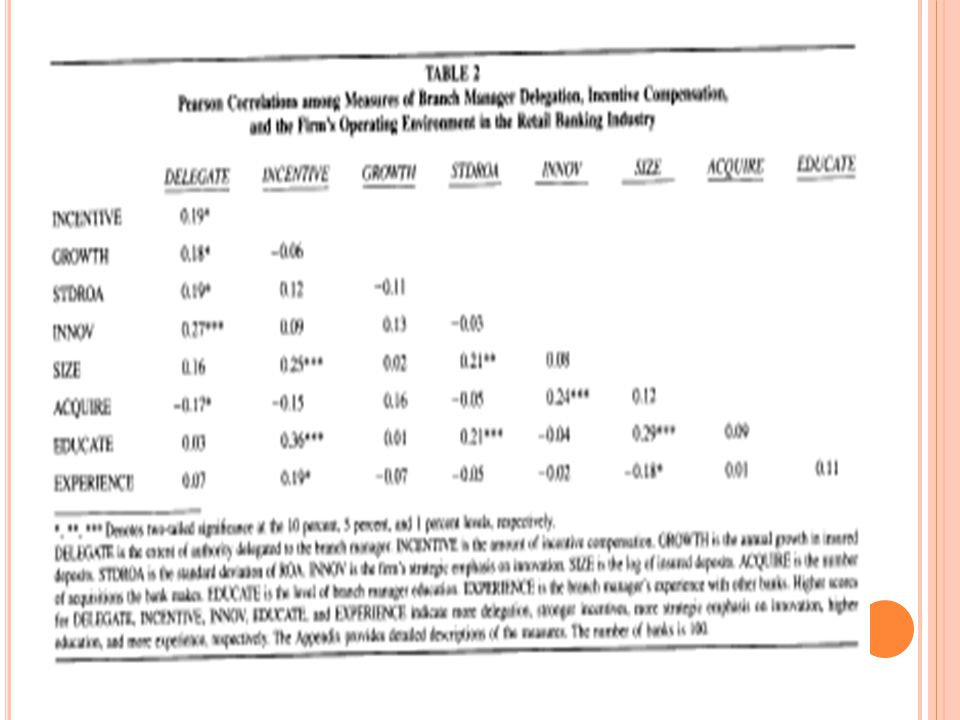

R ESULTS Descriptive Statistics (Table 1) The survey responses incentive compensation delegation firm innovation The Correlations Among the Variables (Table 2) Endogenous variables Exogenous variables

The survey responses incentive compensation delegation firm innovation The Correlations Among the Variables (Table 2) Endogenous variables Exogenous variables")

27

R ESULTS CONT..... The two-stage least squares (2SLS) Delegate Equations (3) : R 2 = 17% Incentive Equations (4) : R 2 = 19% Note: similar to Holthausen et al. (1995, 300) Result indicate (summary): High growth, Volatile, and Innovative Banks Delegate more authority to Branch Managers. Manager with more authority receive more incentive-based pay. The result provide some of the first empirical evidence on the link between the delegation and incentive compensation choices for lower- level managers in a firm.

Delegate Equations (3) : R 2 = 17% Incentive Equations (4) : R 2 = 19% Note: similar to Holthausen et al. (1995, 300) Result indicate (summary): High growth, Volatile, and Innovative Banks Delegate more authority to Branch Managers. Manager with more authority receive more incentive-based pay. The result provide some of the first empirical evidence on the link between the delegation and incentive compensation choices for lower- level managers in a firm..")

29

C ONCLUSIONS Two key organizational design choices: Delegation of authority to lower-level managers The provision of incentive compensation Empirical Study: Examinnes empirically the link between delegation and incentive compensation for branch managers in retail banks.: Result: Incentive pay does not affect the firm’s delegation choice Inconsistent with Agency Theory (incentive compensation is a major cost of delegation)

")

30

C ONCLUSIONS CONT..... Empirical Caveats (Limitations): No empirical study can simultaneously model all organizational design choice abstracts from the endogenity of firm characteristics, such as innovation. Abstract from other reasons for awarding incentive compensation Therefore, this study is a partial equilibrium analysis Organizational design variables such as delegation, the nature of the firm’s operating environment, and managers’ risk aversion are measured with error. The study uses observations from firms in a single industry polled at the same time. The isolation of exogenous variables to identify the simultaneous equation is difficult, and the empirical model is likely misspecified.

: No empirical study can simultaneously model all organizational design choice abstracts from the endogenity of firm characteristics, such as innovation. Abstract from other reasons for awarding incentive compensation Therefore, this study is a partial equilibrium analysis Organizational design variables such as delegation, the nature of the firm’s operating environment, and managers’ risk aversion are measured with error. The study uses observations from firms in a single industry polled at the same time. The isolation of exogenous variables to identify the simultaneous equation is difficult, and the empirical model is likely misspecified..")

31

C ONCLUSIONS CONT..... Important Contribution : This study provides some of the first empirical evidence on the joint nature of the firm’s delegation and incentive compensation choices for lower-level manager.

32

S EKIAN & T ERIMA K ASIH Salemba, 19 Mei 2009

Presentasi serupa