Upload presentasi

Presentasi sedang didownload. Silahkan tunggu

1

DOSEN : ARASY ALIMUDIN,SE,MM

Balanced Scorecard DOSEN : ARASY ALIMUDIN,SE,MM

2

Balanced Scorecard Kaplan dan Norton menguraikan kartu catatan yang seimbang sebagai berikut: " BSC (Kartu catatan yang seimbang) mempertahankan ukuran keuangan tradisional. Tetapi ukuran keuangan menceritakan peristiwa yang lampau, suatu cerita cukup untuk perusahaan industri di mana investasi di dalam hubungan pelanggan dan kemampuan jangka panjang dengan membuat Kritikal sukses. Ukuran keuangan ini adalah tidak cukup,karena untuk memandu dan mengevaluasi dibutuhkan informasi perusahaan untuk menciptakan nilai masa depan melalui investasi dalam pelanggan, para penyalur, karyawan, proses, teknologi, dan inovasi."

mempertahankan ukuran keuangan tradisional. Tetapi ukuran keuangan menceritakan peristiwa yang lampau, suatu cerita cukup untuk perusahaan industri di mana investasi di dalam hubungan pelanggan dan kemampuan jangka panjang dengan membuat Kritikal sukses. Ukuran keuangan ini adalah tidak cukup,karena untuk memandu dan mengevaluasi dibutuhkan informasi perusahaan untuk menciptakan nilai masa depan melalui investasi dalam pelanggan, para penyalur, karyawan, proses, teknologi, dan inovasi.")

3

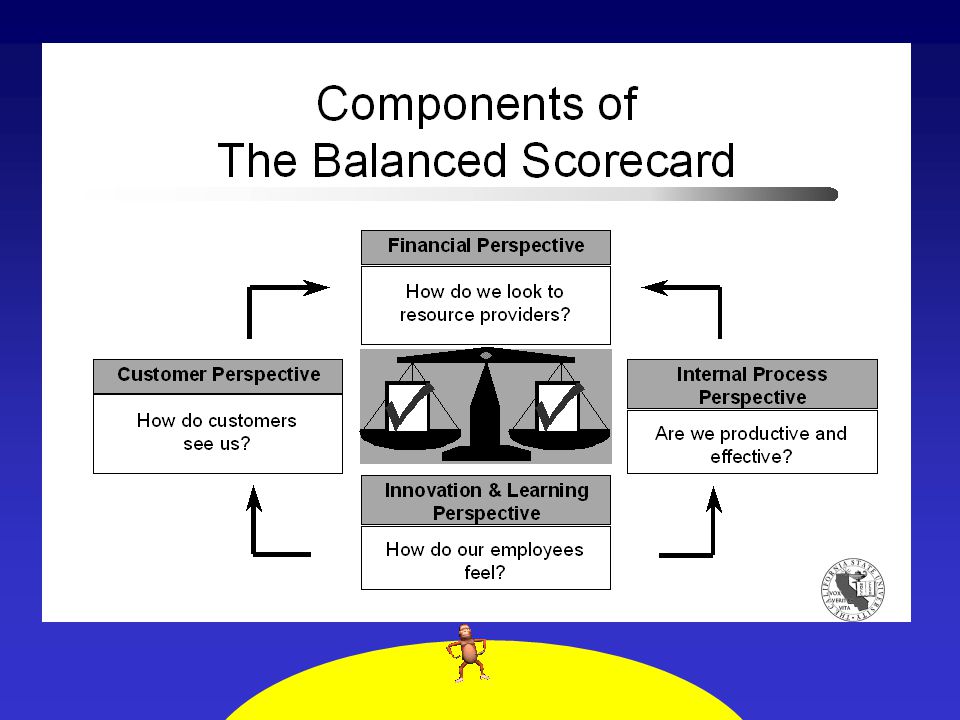

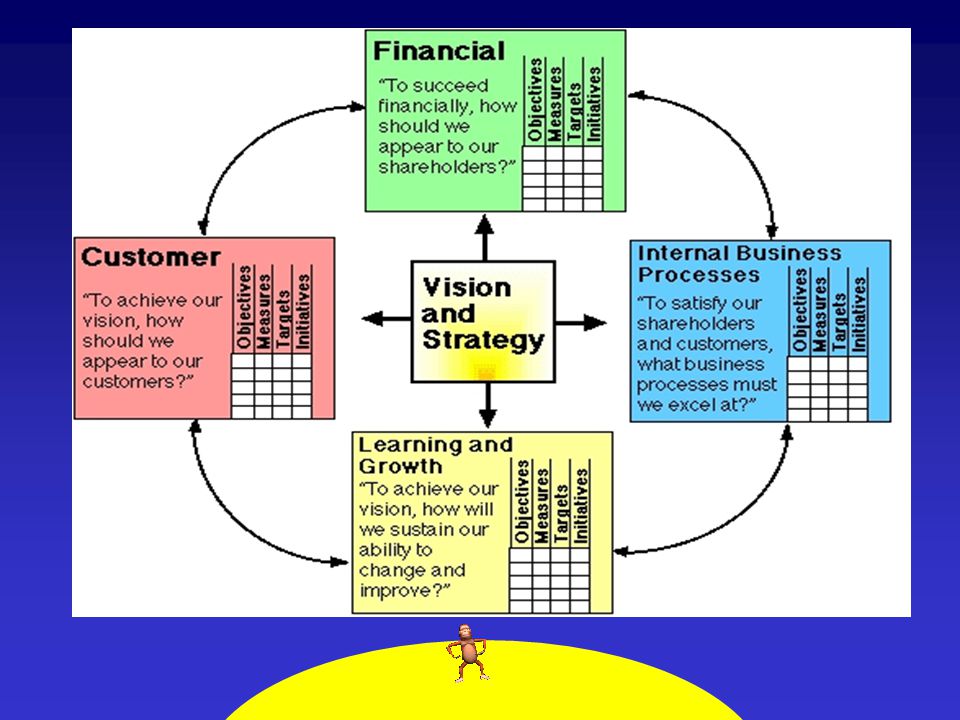

Balanced Scorecard Kartu catatan yang seimbang menyatakan bahwa kita memandang organisasi dari empat perspektif, dan untuk membangun pengukuran , mengumpulkan data dan menelitinya sehubungan dengan masing-masing perspektif meliputi: · Perspektif Pelanggan · Perspektif Proses Bisnis · Perspektif Pelajaran dan Pertumbuhan · Perspektif keuangan

5

Balanced Scorecard Perspektif pelanggan, pelanggan dan segmen pasar di mana bisnis unit akan bersaing dikenali. Ukuran Hasil Inti meliputi kepuasan pelanggan, ingatan pelanggan, didapatnya pelanggan baru, profitabilitas pelanggan, dan penguasaan pasar pada segmen ditargetkan. faktor faktor kritis yang menyebabkan pelanggan setia kepada para produsen/produk juga dimasukkan.

6

Core Customer Measures

Market Share Percent of market segment captured by your organization Percent of each customer's total requirement served by your company (e.g. for customers purchasing clothing at your apparel store, what portion of their total annual clothing budget do they spend with you?) Customer Retention Number of defections (customers who take their business elsewhere) Increase in sales to current customers Frequency of orders / visits / contacts with current customers

Customer Retention. Number of defections (customers who take their business elsewhere) Increase in sales to current customers. Frequency of orders / visits / contacts with current customers.")

7

Core Customer Measures

Customer Acquisition Number of new customers, or total sales to new customers Ratio of sales to inquiries Average cost to acquire a new customer Average order size, or average revenue per customer interaction Customer Satisfaction Number of complaints Number of unsolicited thank you letters Number of individuals indicating that they are extremely satisfied with their experience with your organization on a satisfaction survey

8

Customer Value Proposition Measures

Product / Service Attributes Functionality Overall satisfaction with product / service Number of features exceeding those provided by competitors Quality Service failure index Return rate Number of revisions Warranty claims Price Customer perception of value for money Gross margin Costomer Life – Cycle Cost Customer profitabikity

9

Customer Value Proposition Measures

Product / Service Attributes Timeliness Percent on-time delivery Total time for customer interaction (e.g. time for hotel check-in process) Average waiting time (e.g. line-up for bank teller) Satisfaction with delivery time Image Brand Premium paid for brand name Market share Percent of customers in target market segment

Average waiting time (e.g. line-up for bank teller) Satisfaction with delivery time. Image. Brand. Premium paid for brand name. Market share. Percent of customers in target market segment.")

10

Customer Value Proposition Measures

Relationship Availability Percent of key items out of stock Number of back-orders Shopping Experience Internal evaluations Customer surveys, etc. Total number of visits Convenience Request fulfillment time Number of customer interactions required Customer interaction time required (e.g. express car rental)

")

11

Balanced Scorecard Di dalam perspektif proses bisnis internal para eksekutip harus mengidentifikasi proses internal yang kritis di mana organisasi harus meningkatkan kemampuan untuk menarik dan mempertahankan pelanggan di dalam segmen pasar ditargetkan. BSC menyertakan proses inovasi. Hal ini mengakibatkan pengembangan produksi baru atau jasa

12

Internal Business Process Measures

Identify or Make the Market Profitability by market segment Percent of revenue from new products Percent of revenue from new customers Design Build Time to market Break-even time Number of defects Process time Process Cost

13

Internal Business Process Measures

Deliver Percent on-time delivery Stock-outs Percent defects Service (post-sales) Average satisfaction rating Number of customers re-ordering within a three-month period Number of customers who do not order again within a year Number of deliveries during which a related product or service is cross-sold

Average satisfaction rating. Number of customers re-ordering within a three-month period. Number of customers who do not order again within a year. Number of deliveries during which a related product or service is cross-sold.")

14

Balanced Scorecard perspektif Pembelajaran dan pertumbuhan mengidentifikasi infrastruktur organisasi untuk menciptakan peningkatan dan pertumbuhan jangka panjang. Tujuan keuangan, Pelanggan dan sasaran hasil proses internal akan sering mengungkapkan gap antara kemampuan orang-orang yang ada, sistem dan prosedur dan apa yang akan diperlukan untuk mencapai. Untuk menutup gap ini, organisasi harus menanam modal dalam meningkatkan ketrampilan karyawan, tingkatkan teknologi informasi dan sistem, dan menseragamkan prosedur organisasi dan kegiatan rutin.

15

Learning and Growth Measures

Employee Capabilities Employee satisfaction (involvement, recognition, access to information, support from staff functions, etc.) Staff turnover Productivity (revenue per employee, return on compensation, profit per employee, etc.) Number of employees qualified for key jobs relative to anticipated requirement Information Technology Information coverage ratio - number of processes having adequate information on quality, cycle time, and cost Percent of customer information available during front-line interactions Return on data - new revenue per database etc.

Staff turnover. Productivity (revenue per employee, return on compensation, profit per employee, etc.) Number of employees qualified for key jobs relative to anticipated requirement. Information Technology. Information coverage ratio - number of processes having adequate information on quality, cycle time, and cost. Percent of customer information available during front-line interactions. Return on data - new revenue per database etc.")

16

Learning and Growth Measures

Motivation and Alignment Suggestions received Suggestions implemented Rewards provided Length of time required to improve a key measure such as on-time deliveries by 50% (half-life metric) Percent of employees with objectives aligned with key Balanced Scorecard measures

Percent of employees with objectives aligned with key Balanced Scorecard measures.")

17

Balanced Scorecard Prespektif Keuangan melalui ukuran keuangan seperti pendapatan usaha, laba modal mempekerjakan, nilai tambah ekonomi dll

18

Financial Measures Revenue Growth Sales and market share

Number of new products, or new applications of existing products and services Number of new customers and markets Number of new market channels, differentiating on service, delivery mode and price Number of new pricing strategies Cost Management Revenue per employee Unit cost reduction Percent use of low cost business processes. (e.g. increase use of EDI to replace costly manual purchasing approaches) Percentage of expenses measured by Activity Based Costing

Percentage of expenses measured by Activity Based Costing.")

19

Financial Measures Asset Utilization

Inventory reduction, increased turns Cash-to-cash cycle Return on capital Productivity / efficiency

21

Proses dalam penyusunan BSC

Langkah 1 : Pilih Target Segmen Stakeholders Lang 2: Identifikasi kebutuhan mereka Masing-Masing segmen pelanggan ditandai oleh satuan kebutuhan yang unik Lang 3: Tentukan gap Performance ( perspektif eksternal) Lang 4: prioritas peningkatan yang di-set Stakeholder Lang 5: Hubungkan kebutuhan stakeholder ke proses internal

Lang 4: prioritas peningkatan yang di-set. Stakeholder. Lang 5: Hubungkan kebutuhan stakeholder ke. proses internal.")

22

Proses dalam penyusunan BSC

Lang 6 : mengidentifikasi hubungan dari tiap proses di dalam organisasi dengan kunci kebutuhan stakeholder Lang 7: Tetapkan proses peningkatan prioritas ( perspektif internal) Lang 8: Menetapkan pengembangan pengukuran dan gol untuk prioritas peningkatan proses BSC Lang 9 : Meningkatkan Proses Kritis Individu yang terlibat Lang 10: Menaksir kembali strategi

Lang 8: Menetapkan pengembangan. pengukuran dan gol untuk. prioritas peningkatan proses BSC. Lang 9 : Meningkatkan Proses Kritis Individu yang. terlibat. Lang 10: Menaksir kembali strategi.")

23

Terima Kasih

Presentasi serupa

>")

>")

Pertemuan 16>")