Upload presentasi

Presentasi sedang didownload. Silahkan tunggu

1

Depreciation, Impairments, Depletion

2

Depreciation Depresiasi adalah proses akuntansi dari alokasi kos aset tetap ke biaya dengan cara rasional dan sistematis pada periode dimana diharapkan mendapat manfaat dari pemakaian aset tersebut Alokasi biaya aset tetap: Aset berumur panjang = biaya depresiasi; Intangible = biaya amortisasi Sumberdaya mineral = biaya deplesi

3

Metode Depresiasi Metode yang dipakai harus ‘sistematis dan rasional’:

Activity method (unit dipakai atau produksi); Straight-line method Diminishing (accelerated)-charge method; Sum-of-the-years’-digits. Declining-balance method

; Straight-line method. Diminishing (accelerated)-charge method; Sum-of-the-years’-digits. Declining-balance method.")

4

Contoh PT Kotabaru bergerak di bidang pertambangan memiliki mesin dengan yang dibeli tahun 2008 seharga $ , perkiraan Umur Ekonomis 5 tahun, nilai residu $50.000, dan umur produktif jam. Hitunglah biaya depresiasinya:

5

Revaluasi PSAK 16 mengharuskan memakai nilai wajar untuk revaluasi

Kenaikan jumlah tercatat neto (surplus revaluasi) dikredit ke dana pemegang saham ‘cadangan surplus revaluasi’ Perlakuan dampak revaluasi: Penyajian kembali secara proporsional; Revaluasian neto dan penghapusan akumulasi penyusutan dicatat sebagai jumlah tercatat bruto baru

dikredit ke dana pemegang saham ‘cadangan surplus revaluasi’ Perlakuan dampak revaluasi: Penyajian kembali secara proporsional; Revaluasian neto dan penghapusan akumulasi penyusutan dicatat sebagai jumlah tercatat bruto baru.")

6

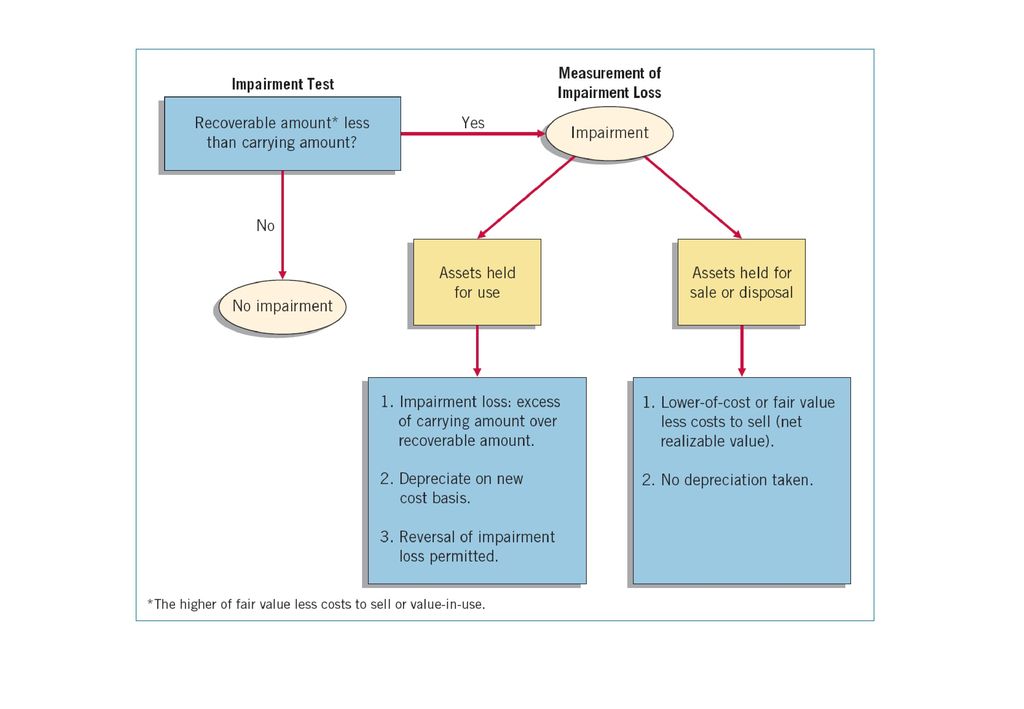

Impairments Impairment dilakukan ketika perusahaan tidak mampu memulihkan jumlah nilai tercatat aset baik melalui pemakaian ataupun penjualan suatu aset berumur panjang

7

Contoh Impairments PT Kotabaru memiliki mesin di 31/12/2011 seharga Rp26.000, akumulasi penyusutan sebesar Rp perkiraan Umur Ekonomis 4 tahun, nilai residu Rp2.000, dan nilai terpulihkan sebesar Rp Buatlah jurnal yang diperlukan! Jika PT Kotabaru memperkirakan aliran kas mendatang sebesar Rp6.000 per tahun dan nilai residunya Rp1.000 dengan tingkat diskon 8%, buatlah jurnal yang diperlukan!

8

Jawab Loss on Impairment Rp3.000

Rp Impairment Loss Rp14.000 Rp11.000 Loss on Impairment Rp3.000 Accumulated Depreciation—Equipment Rp3.000

9

Jawab Peralatan Rp26.000 (-) Akumulasi Depresiasi peralatan 15.000

Carrying value (Dec. 31, 2011) Rp11.000 Depreciation Expense Rp5.500 Accumulated Depreciation—Equipment Rp5.500

Rp Depreciation Expense Rp Accumulated Depreciation—Equipment Rp")

11

Depletion Sumberdaya alam dibagi menjadi: Aset Biologis;

Sumberdaya mineral Perhitungan deplesi berdasarkan komponen: Pre-exploratory costs. Exploratory and evaluation costs. Development costs.

12

Write-off of Resource Cost

Normally, companies compute depletion on a units-of-production method (activity approach). Depletion is a function of the number of units extracted during the period. Calculation: Total cost – Residual value = Depletion cost per unit Total estimated units available Units extracted x Cost per unit = Depletion

. Depletion is a function of the number of units extracted during the period. Calculation: Total cost – Residual value. = Depletion cost per unit. Total estimated units available. Units extracted x Cost per unit. = Depletion.")

13

Contoh Illustration: MaClede Co. acquired the right to use 1,000 acres of land in South Africa to mine for silver. The lease cost is $50,000, and the related exploration costs on the property are $100,000. Intangible development costs incurred in opening the mine are $850,000. MaClede estimates that the mine will provide approximately 100,000 ounces of silver. Illustration 11-18

14

Contoh (lanjutan) If MaClede extracts 25,000 ounces in the first year, then the depletion for the year is $250,000 (25,000 ounces x $10). Inventory 250,000 Accumulated Depletion 250,000 MaClede’s statement of financial position: Depletion cost related to inventory sold is part of cost of goods sold.

Presentasi serupa

>")